This blog gives investors more financial information for very smart investing!

Monday, November 23, 2015

Markets edge higher as corporate profits fall

Dow rose 31, advancers over decliners 3-2 & NAZ gained 18. The MLP index was flat at 301 & the REIT index added 1+ to the 322s. Junk bond funds did little & Treasuries dropped. Oil fell into the 39s & gold.keeps sliding lower near multi year lows.

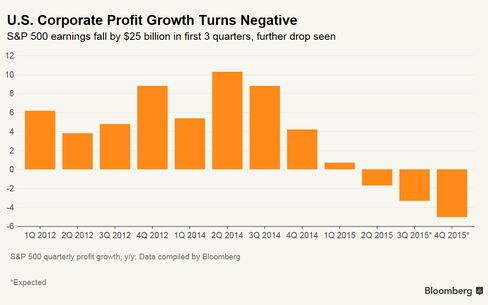

Profits from S&P 500 companies have fallen by $25B

in Q1-Q3, & a further drop is expected

before the end of 2015 as energy companies battle with lower oil prices & a sharp rally in the dollar hits exporters.

About

96% of S&P 500 companies have reported 3Q results so far, & their aggregate net income from continuing operations for Q1-Q3 is $804B, compared with $828B for the same period last year. The aggregate revenue for S&P 500 companies has fallen by $287B over the same period last year. On

a share-weighted basis, S&P 500 profits were down 3.3% in Q3, making this earnings season the worst since

2009, & marking a 2nd consecutive quarter of negative earnings

growth. The energy sector has seen the biggest damage, hurt by

plummeting oil prices. Earnings in the sector have dropped 57% in

Q3 year-over-year. The negative trend in US

earnings is set to persist in Q4, with analysts

expecting a 5% drop in S&P 500 profits in 4Q. Changes in US import prices usually lead profitability by

about 12 months, & without a reversal in the dollar's rally, an

industrial profit recession looks looks to be baked in the cake for 2016.

Federal Reserve Governor Daniel Tarullo said economic data received

since the central bank met in Sep had been mixed, as continued low

US inflation tempered his enthusiasm over progress made this year in

lowering unemployment. “The U.S. economy seems still to be

chugging along with modestly above-trend growth,” Tarullo said. “We’ve certainly seen continued

improvement in the labor market, but the environment for inflation is

still one where there is still a lot of uncertainty.” Policy makers are widely expected to increase their benchmark

federal funds rate by a quarter percentage point on Dec 16. "Some of the fears that many people held in the August and early September period have not been realized," Tarullo said. "Having said that, I think it’s still mixed picture." The

Fed’s preferred gauge for inflation has been below the central bank’s 2% target for more than 3 years & registered 0.2% in

the 12 months thru Sep. Some Fed officials have argued that inflation will move back up

close to 2% as the transitory effects of a strengthened dollar & oil’s price plunge fade. Tarullo isn't in that camp. “Others,

myself included, have thought it might be better to wait for some more

tangible evidence that we’re going in that direction” on inflation, he

said. He pointed to market-based & survey-based measures of inflation expectations, saying both had fallen to “historic lows.”

Economic activity in the euro area hit a 4½ year high this month,

according to a new report that also pointed to weak price pressures. A

composite index of services & manufacturing rose to 54.4 from 53.9 in

Oct, Markit Economics said. That’s the

highest reading since May 2011. The individual readings for both

industries climbed, defying expectations for no change.

Levels above 50 signify expansion. The survey points to continued

growth in the 19-nation euro area, where ECB pres

Mario Draghi has said more stimulus may be needed to revive inflation.

Still, there’s little comfort from Markit on that aspect of the economy,

with the latest report showing output prices fell for a 9th month

this year.

“The

central bank remains disappointed with the strength of the upturn at

this stage of the recovery,” said

Markit. “November’s slightly improved PMI reading will no doubt do

little to dissuade policy makers that more needs to be done.” The Markit report showed

“ongoing deflationary pressures” in the euro region. Average input costs

barely rose, linked primarily to falling global commodity prices. In

Germany, the area’s largest economy, Markit’s composite index of

activity rose to 54.9 in Nov, the highest since Aug, from 54.2.

France’s gauge slipped to 51.3 from 52.6. Services growth cooled, with

hotels & restaurants reporting a negative impact from the terrorist

attacks in Paris.

Political chaos around the globe & declining profits did not upset traders. Optimism is running high. Maybe holiday is coming early in the markets. But reality is negative & it has the potential to bring on more selling. Dow is scarcely up YTD.

No comments:

Post a Comment