Dow gave up 24, advancers over decliners 2-1 & NAZ gained 7. The MLP index went up 1+ to the 314s & the REIT index added 2+ to the 367s. Junk bond funds were mixed & Treasuries were purchased. Oil was higher today after a difficult month (see below) & gold shot up on financial uncertainties around the globe.

AMJ (Aleria MLP Index tracking fund)

![Live 24 hours gold chart [Kitco Inc.]](http://www.kitco.com/images/live/gold.gif?0.1464350948328348)

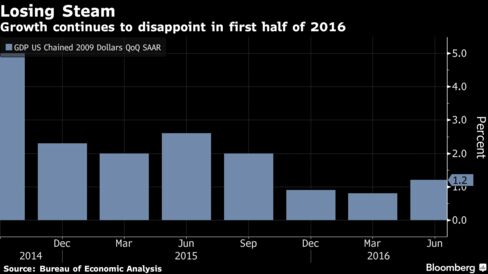

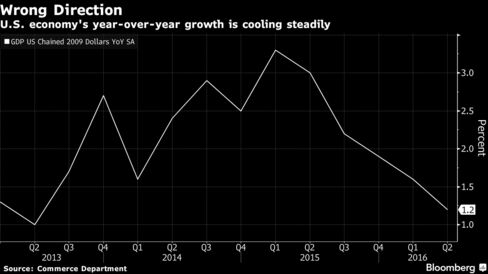

Federal Reserve Bank of San Francisco pres John Williams played down a “low” reading on Q2 US growth & said the economy could still warrant as many as 2 interest-rate increases this year, or none. “There’s definitely a data stream that could come through in the next couple of months that I think would be supportive of two rate increases,” Williams said. “There’s data that we could get that wouldn’t be supportive of that -- it could be one, maybe, or none. Time will tell.” Williams was the first Fed official to speak publicly since policy makers held interest rates steady on Wed for the 5th straight time. The Fed was slightly more upbeat about the US economy in a statement released after its meeting, taking a step toward an increase later this year without signaling how soon a move might come. “The GDP number for the second quarter was low,” said Williams, who isn’t a voting member of the FOMC this year. “Final sales actually looked pretty good,” though, and “a lot of the second-quarter weakness, part of it was really inventory swings.” He also said that the inflation data “was more or less what I had been expecting,” while the effects on the US economy from the Brexit vote appeared to be “very modest.”

Oil prices steadied today amid short-covering after a week-long selloff but were on track to end the month about 15% lower on persistent glut concerns, with the biggest decline seen for US crude in a year. Slower economic growth & high inventories in crude & refined oil products have pressured crude futures some 20% lower from their 2016 highs, technically placing both in bear market territory. The 2 benchmarks hit Apr lows today before paring losses on what traders described as short-covering by investors taking profit on bearish bets placed over the past week. A 3-week low in the $ also supported oil, making commodities denominated in the greenback, such as crude, more affordable to holders of the € & other currencies. Brent's expiring front-month contract was at $42.15, down 1.3% on the day & 15.2% on the month. WTI's Sep contract rose 8¢ to $41.22 a barrel, after slipping earlier to below $41 the first time since Apr 20. The monthly loss of 14.7%t, is the biggest since Jul 2015. Crude prices are still up more than 55% from 12-year lows of $26-$27 in Q1. The recovery faded after prices above $45 enticed more oil drillers to return to the well pad. Drillers added 3 rigs to raise the U.S. oil rig count for a 5th straight week this week. Cheap crude also has led refiners to produce more fuel worldwide, adding to a bloated market. Weaker-than-expected US economic growth also cast a shadow on oil consumption growth. Analysts in a survey published today said they expected higher oil prices this year based on demand growth.

Oil Steadies but U.S. Crude Faces Biggest Monthly Loss in a Year

ExxonMobil, a Dow stock & Dividend Aristocrat, results in Q2 were disappointing. But there were some promising signs, like higher oil prices, but they weren't enough to offset the other issues plaguing the industry. Here's a quick recap of results.

Results

After upstream earnings fell into the loss column in Q1, the company saw a modest pickup to a result that was just barely profitable. The reason for the gain was mostly the uptick in oil prices, because natural gas prices & overall production actually slipped a bit compared to Q1. But total refinery throughput & product sales were down only very slightly. The big difference was refining margin. Total cash from operations & asset sales was $5.5B, enough to cover the $5.1B in capital spending for the qtr. Oil & gas production remained flat compared to the same time last year. The div was increased 2.7% to 75¢ per share. The stock fell 1.25. If you would like to learn more about XOM, click on this link;

club.ino.com/trend/analysis/stock/XOM?a_aid=CD3289&a_bid=6ae5b6f7

It is difficult to make much sense out of trading on the last day of the month. But Dow had a good month, rising 400 to near record highs even though economic data has been drab. Aug will prove if there are legs on this rally. I don't think so.

Dow Jones Industrials

AMJ (Aleria MLP Index tracking fund)

Crude Oil Sep 16

| 41.49 | 0.35 | 0.9% |

Federal Reserve Bank of San Francisco pres John Williams played down a “low” reading on Q2 US growth & said the economy could still warrant as many as 2 interest-rate increases this year, or none. “There’s definitely a data stream that could come through in the next couple of months that I think would be supportive of two rate increases,” Williams said. “There’s data that we could get that wouldn’t be supportive of that -- it could be one, maybe, or none. Time will tell.” Williams was the first Fed official to speak publicly since policy makers held interest rates steady on Wed for the 5th straight time. The Fed was slightly more upbeat about the US economy in a statement released after its meeting, taking a step toward an increase later this year without signaling how soon a move might come. “The GDP number for the second quarter was low,” said Williams, who isn’t a voting member of the FOMC this year. “Final sales actually looked pretty good,” though, and “a lot of the second-quarter weakness, part of it was really inventory swings.” He also said that the inflation data “was more or less what I had been expecting,” while the effects on the US economy from the Brexit vote appeared to be “very modest.”

Fed’s Williams Says Two Rate Increases Still Possible in 2016

Oil prices steadied today amid short-covering after a week-long selloff but were on track to end the month about 15% lower on persistent glut concerns, with the biggest decline seen for US crude in a year. Slower economic growth & high inventories in crude & refined oil products have pressured crude futures some 20% lower from their 2016 highs, technically placing both in bear market territory. The 2 benchmarks hit Apr lows today before paring losses on what traders described as short-covering by investors taking profit on bearish bets placed over the past week. A 3-week low in the $ also supported oil, making commodities denominated in the greenback, such as crude, more affordable to holders of the € & other currencies. Brent's expiring front-month contract was at $42.15, down 1.3% on the day & 15.2% on the month. WTI's Sep contract rose 8¢ to $41.22 a barrel, after slipping earlier to below $41 the first time since Apr 20. The monthly loss of 14.7%t, is the biggest since Jul 2015. Crude prices are still up more than 55% from 12-year lows of $26-$27 in Q1. The recovery faded after prices above $45 enticed more oil drillers to return to the well pad. Drillers added 3 rigs to raise the U.S. oil rig count for a 5th straight week this week. Cheap crude also has led refiners to produce more fuel worldwide, adding to a bloated market. Weaker-than-expected US economic growth also cast a shadow on oil consumption growth. Analysts in a survey published today said they expected higher oil prices this year based on demand growth.

Oil Steadies but U.S. Crude Faces Biggest Monthly Loss in a Year

ExxonMobil, a Dow stock & Dividend Aristocrat, results in Q2 were disappointing. But there were some promising signs, like higher oil prices, but they weren't enough to offset the other issues plaguing the industry. Here's a quick recap of results.

Results

| Q2 2016 | Q1 2016 | Q2 2015 | |

|---|---|---|---|

| Revenue (M) | $57,694 | $48,707 | $74,113 |

| Net income (M) | $1,700 | $1,810 | $4,190 |

| EPS | 41¢ | 43¢ | $1.00 |

After upstream earnings fell into the loss column in Q1, the company saw a modest pickup to a result that was just barely profitable. The reason for the gain was mostly the uptick in oil prices, because natural gas prices & overall production actually slipped a bit compared to Q1. But total refinery throughput & product sales were down only very slightly. The big difference was refining margin. Total cash from operations & asset sales was $5.5B, enough to cover the $5.1B in capital spending for the qtr. Oil & gas production remained flat compared to the same time last year. The div was increased 2.7% to 75¢ per share. The stock fell 1.25. If you would like to learn more about XOM, click on this link;

club.ino.com/trend/analysis/stock/XOM?a_aid=CD3289&a_bid=6ae5b6f7

Higher Oil Prices Weren't Enough to Lift ExxonMobil's Second-Quarter Earnings

Exxon Mobil (XOM)

It is difficult to make much sense out of trading on the last day of the month. But Dow had a good month, rising 400 to near record highs even though economic data has been drab. Aug will prove if there are legs on this rally. I don't think so.

Dow Jones Industrials