This blog gives investors more financial information for very smart investing!

Thursday, July 14, 2016

Markets climb higher on economic data

Dow advanced 153, advancers over decliners better than 2-1 & NAZ went up 33. The MLP index crawled up a fraction to 321 & the REIT index slid back 1+ to 370 (essentially at its record reached yesterday). Junk bond funds were a little higher & Treasuries were sold today. Oil rose & gold declined.

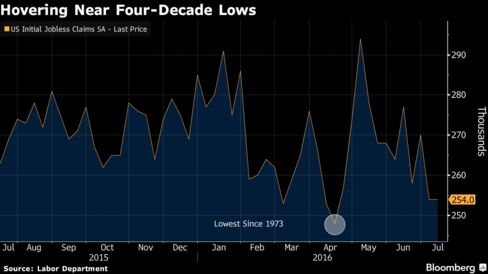

The number of applications for US unemployment benefits last week

held at the lowest level since mid-Apr, further evidence of a strong

labor market. Jobless claims were unchanged at 254K according to a Labor Dept.

The estimate called for filings to

increase to 265K. In Apr, applications dropped to a 4-decade low

of 248K.

Companies

having trouble finding qualified & skilled workers are hesitant to

dismiss employees as demand shows signs of picking up after a weak start

to the year. Weekly claims have been below 300K for 71 straight

weeks, the longest period since 1973 & consistent with robust

employment conditions. Claims

data in Jul typically can be volatile as automakers begin the process

of temporarily shutting down plants to retool for the new model year. Because of such seasonal events, economists tend to focus

on a rolling monthly average that smoothes out the weekly fluctuations.

The 4-week average of claims declined to 259K, the lowest since

Apr, from 264K in the prior week. The

number continuing to receive jobless benefits rose 32K

to 2.15 & the unemployment rate among

those eligible for benefits increased to 1.6%.

JPMorgan, a Dow stock, Q2 profit fell 1.4%, beating estimates as

fixed-income trading revenue & loan growth jumped. EPS was $1.55 versus $1.54 a year earlier. Excluding an

accounting adjustment & a legal benefit, EPS was $1.46%, 3¢ better than analyst the estimate.

Revenue

climbed 2.8% to $25.2B, beating the $24.5B

estimate &

average core loans increased 16% from a year earlier. The revenue

figure included $3.96B from fixed-income trading, a 35% increase, beating the $3.57B estimate. The firm cited

strength in rates, currencies, emerging markets, credit & securitized

products. Equity trading rose 1.5% to $1.6B. Earnings at the corp & investment bank

climbed 6.5% to $2.49B as revenue rose 5.1% from a

year earlier. Markets revenue, which includes bond % stock trading,

rose 23%. Investment

banking revenue fell 15% to $1.5B on lower

equity-underwriting fees (in line with the $1.49B estimate). Profit from consumer & community banking rose 4.9% to $2.66B on strength in

mortgages. Revenue was $11.5B, up 4% from a year earlier. Net

income in asset management increased 16% to

$521M on lower legal expenses. Revenue fell 7.4% to $2.94B on weaker markets & lower performance fees. Commercial

banking posted a 33% profit increase

to $696M on higher loan balances. The stock rose 1.74.

Wholesale prices in the US rose more than forecast in Jun, paced by the biggest jump in fuel costs in a year. The

producer-price index gained 0.5%, the most since May 2015, after

a 0.4% rise the prior month, according to the Labor Dept. The forecast was for a 0.3% advance. Costs rose 0.3% over

the past 12 months, the biggest year-to-year gain since Dec 2014. As

energy costs stabilize & the restraining influence of a strong $

dissipates, a slowly improving economy will probably lead to a more

sustained pickup in price pressures. Federal Reserve officials are

monitoring inflation’s progress toward their goal as they consider when

to lift interest rates again. Energy

expenses jumped 4.1%, the biggest gain since May 2015, with

gasoline increasing 9.9% & food prices rose 0.9 percent, the most

since Jan. Excluding food & energy, wholesale prices climbed 0.4% following a 0.3% advance the prior month. Those costs were up 1.3% from

Jun 2015. Excluding food & energy & also eliminating trade

services, producer costs rose 0.3% after falling 0.1% the

previous month. Some prefer this reading because it strips

out the most volatile components of PPI. One exception to the

otherwise strong readings was medical care costs which were little

changed in Jun before adjusting for seasonal variations following,

according to the report. These figures are used to calculate healthcare

expenses in the Commerce Dept consumer spending inflation index,

the Fed's preferred price measure. Those prices have climbed just 1.1% in the past 12

months, the smallest year-to-year gain since Dec.

The bulls remain in command of the stocks market, but keep in mind that it is vastly overbought. When Dow rise more than 1K in a couple of weeks, that spells correction time. A very big unknown is how the British exit from EIU will play out. The effects will be global. Additionally, this is the start of earnings season. Hang on for what may be a bumpy ride for stocks.

No comments:

Post a Comment