This blog gives investors more financial information for very smart investing!

Monday, July 18, 2016

Higher markets after global turmoil

Dow gained 28, advancers over decliners almost 2-1 & NAZ went up 33. The MLP index was even at 321 & the REIT index rose 1 to the 369s (in record territory). Junk bond funds were a little higher & Treasuries inched up. Oil dropped a big 1 & gold went up.

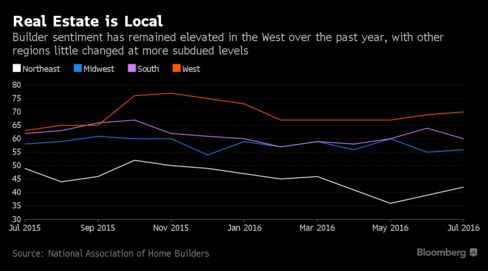

Confidence among US homebuilders declined in Jul from a 5-month

high, showing the construction industry remains in a slow, if

unspectacular, recovery as the busiest part of the selling season comes

to a close, according to the National Association of

Home Builders/Wells Fargo. Builder sentiment gauge declined to 59 from 60. The forecast was for it to hold at 60; readings

greater than 50 indicate more respondents reported good market

conditions. The gauge of prospective buyer traffic declined to 45 from 46 & the measure

of 6-month sales outlook decreased to 66 from from a 7-month high

of 69, while index of current sales fell 1 point to 63.

The NAHB index has held within a narrow range of 58 to 61 this year,

signaling builders are generally positive about the outlook although

there has been little additional momentum to propel sentiment to a

higher level. Ultra-low mortgage rates, employment gains & a growing

number of households as younger Americans start families will feed

demand for housing, while slow wage growth & memories of the

industry's collapse during the last recession remain restraints. The

index reached a low of 8 in Jan 2009 & a high of 78 in 1998.

Economists predict the ECB will keep

policy unchanged on Thurs but announce fresh measures before the end

of the year, probably in Sep along with updated forecasts.

Officials meet a week after the Bank of England opted not to cut rates

in the immediate wake of the UK vote to quit the EU,

instead saying it will probably ease in Aug. Of those saying the

ECB will add stimulus eventually, 97% expect it will extend bond

buying past Mar 2017, almost 40% said it’ll cut the deposit

rate & less than 20% envisage higher monthly QE purchases.

Bank of America quarterly profit fell as the lender was hurt by the continued drag of low

interest rates, though the bank's results beat expectations. EPS was

36¢, down from 45¢ last year. The latest results included 6¢ in market-related charges. Analysts had

expected the bank to earn 33¢. Revenue fell to $20.4B from $21.96B a year ago. Adjusted

revenue was $20.6B, above the $20.41B expected. Trading revenue, excluding an accounting adjustment, rose 12% to $3.7B from $3.32B in Q2 last year. Net interest income fell 12% to $9.21B from $10.46B a year ago. Expenses declined 3.3% to $13.49B from $13.96B a year

ago. The bank continued to cut jobs & sell or shutter branches. Things have been relatively calm for the bank. Last month, it passed the Federal Reserve's stress test

without incident for the first time since 2013. The crisis-era legal

fees that dogged earnings have been receding for a couple years. The stock rose 21¢. If you would like to learn more about BAC, click on this link: club.ino.com/trend/analysis/stock/BAC?a_aid=CD3289&a_bid=6ae5b6f7

The bull were not greatly disturbed by growing global turmoil. One explanation, in chaos there is opportunity. But this is not the right way to make money in the stock market. The popular averages are at or near record highs which will not last if unsettled conditions grow worse.

No comments:

Post a Comment