This blog gives investors more financial information for very smart investing!

Wednesday, July 6, 2016

Markets drift lower on growth worries

Dow dropped 90, decliners over advancers more than 2-1 & NAZ declined 13. The MLP index fell 3+ to 310 & the REIT index slid back 1+ to the 364s. Junk bond funds did little & Treasuries were a little lower after recent price gains. Oil was off slightly & gold continued rising to new heights.

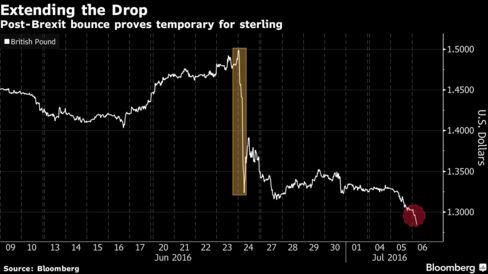

The £ sank to a fresh 31-year low as the fallout from Britain's

vote to leave the EU continued to reverberate thru

financial markets. The currency fell beyond $1.28, 4¢ below its weakest point the day after the nation's Jun 23

referendum, before paring its decline. The ¥ climbed a good 1.3% against all 16 of its major counterparts as investors sought

havens from the turmoil that's also weighing on global stocks.

The

£ has tumbled to 3-decade lows for the past 2 days amid

mounting evidence the Brexit vote is hurting confidence the British

economy. M&G Investments suspended a £4.4B ($5.7B) real-estate fund Tues, following on the heels of Aviva

Investors & Standard Life Investments after a flurry of redemption

requests. With the real estate tremors & fund suspensions echoing the

start of the 2007 financial crisis, concern is building that a failure

to control the aftershocks of the referendum will propel the nation into

a recession.

American service providers expanded in Jun at the fastest pace in 7 months on stronger orders & sales that signal a healthy US

economy. The Institute for Supply Management non-manufacturing index jumped

to 56.5, exceeding the most optimistic projection,

from 52.9 in May. The gauge from construction firms to retailers

posted its biggest monthly advance since Feb 2008, helped by

resilient consumer spending. Combined with an already reported pickup in

manufacturing, the data suggest the US economy was gaining speed

leading up to Britain's decision to exit the EU. The ISM factory survey published last week indicated that a nascent

recovery in the beleaguered manufacturing industry also may be taking

shape. That index climbed to 53.2, the highest level since Feb 2015,

boosted by stronger bookings & production. Details from the services survey showed the new

orders index climbed to 59.9 from 54.2. The increase was the biggest since Mar 2010 & shows the

economy caught a spark as Q2 drew to a close. The business activity index, which parallels the ISM factory production gauge, increased to 59.5 from 55.1. A measure of non-manufacturing employment advanced to 52.7

from 49.7 the prior month, indicating more companies are adding workers. The ISM supplier-deliveries index rose to 54 last month, the highest

in more than a year, from 52.5. A reading above 50 means deliveries

slowed, which is a positive signal as it indicates companies had trouble

keeping up with demand.

The US trade deficit widened in May by the most in nearly a year as

exports fell & a pickup in domestic demand led to more imports of

consumer goods & industrial materials. The gap grew by 10.1%, the most since Aug 2015, to $41.1B from the prior

month, according to the Commerce Dept. The forecast called for a $40B shortfall. American

companies imported more cars, mobile phones, apparel & industrial

supplies as the economy started to strengthen after a Q1 lull. At the same time, overseas sales of US goods face

hurdles including weak global markets, with Britain's vote to leave the

EU clouding the outlook. The

merchandise trade deficit with the EU jumped 12.8% to $13.4B, a month before Brexit. US goods exports to the region

fell 4.2%. The good news was that the US

petroleum deficit fell to $2.9B in May, the smallest since

Feb 1999. Oil prices rose $4.71 a barrel during the month, the biggest advance in 5 years.

Exports

decreased 0.2% to $182.4B on less demand for aircraft,

computers, industrial machines & auto parts. Imports climbed 1.6% to $223.5B. While

shipments of goods made overseas rose to a 3-month high, imported

services climbed to the highest on record. After

eliminating the influence of prices, used to

calculate GDP, the trade deficit expanded to a 3-month high of $61.1B from $57.5B. Revised data

released last week showed the Q1 trade gap actually

narrowed rather than widened as previously estimated. The May report also showed the

merchandise trade gap with China,

widened 19.4% to $29B.

Stocks are having another tough day. Enthusiasm from last week is gone & the outlook for news stories is not good. The jobs report on Fri will probably be so-so, although it should not affect how Janet thinks about maintaining low interest rates. Alcoa (AA) will report earnings Fri evening which kicks off earnings season. This could be a difficult month for the stock market.

No comments:

Post a Comment