This blog gives investors more financial information for very smart investing!

Friday, July 29, 2016

Markets drift lower on weak GDP data

Dow was down 35, advancers a little ahead of decliners & NAZ added 1. The MLP index fell 2+ to the 312s & the REIT index rose 4 to the 376s. Junk bond funds were flattish & Treasuries went up. Oil has fallen to just above 40 & gold gained again.

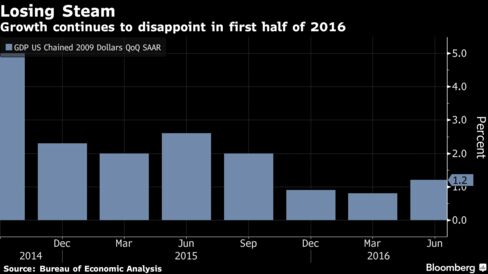

The US economy expanded less than forecast in Q2

after a weaker start to the year than previously estimated as companies

slimmed down inventories & remained wary of investing amid shaky

global demand. GDP rose at a 1.2%

annualized rate after a 0.8% advance the prior qtr, according to the Commerce

Dept. The forecast called for a 2.5%

increase. The report raises the risk to the outlook at a time

Federal Reserve policy makers are looking for sustained improvement.

While consumers were resilient, businesses were cautious,

cutting back on investment & aggressively reducing stockpiles amid

weak global markets, heightened uncertainty and the lingering drag from a

stronger dollar.

Private

fixed investment, which includes residential & business spending,

dropped at a 3.2%, the most in 7

years. The Commerce Dept also issued

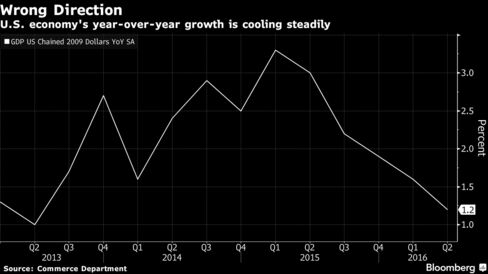

its annual revisions. The Q1 reading was revised from a previously reported 1.1% gain. The

new breakdown shows a more pronounced slowdown in the economy heading

into 2016. Year-over-year growth rate cooled from 3.3% in

last year's Q1 to 1.9% in Q4-2015, rather than the previous downshift from 2.9% to 2%. The

easing in growth continued into H1 of this year. The

year-over-year pace for Q1-2016 was revised down to

1.6% from 2.1%. That revised

trajectory has implications for Fed officials, as they’re faced with an

expansion that has been steadily losing steam. The report also showed that in Q2, GDP expanded at a 1.2% rate from the same period a year earlier.

The growth estimate is the first of 3 for the

qtr.

Consumer confidence slid in Jul from the prior month on dimmer

views of the US economy's prospects & lingering concerns among

higher-income earners about global market conditions. The University of Mich said that its final index of

sentiment declined to 90 this month from 93.5 in Jun. The

projection was for a reading of

90.2 after the preliminary Jul figure of 89.5. A record share of households with incomes in the top 1/3 mentioned

the UK decision to leave the EU was weighing on

outlooks. The gap between current views of the economy and expectations

last month widened in Jul. “While concerns about Brexit are likely to quickly recede, weaker

prospects for the economy are likely to remain,” Richard Curtin, the survey’s director, said. The sentiment survey's current conditions index, which measures

Americans’ assessment of their personal finances, fell in Jul to 109

from 110.8 last month & the measure of expectations six months from now

decreased to 77.8 from 82.4. Americans anticipated an inflation rate of 2.7% in the next

year, up from 2.6% in Jun. They expect prices to rise 2.6% over the next 3-10 years, the same as in the previous

month. Despite the setback in sentiment this month, consumers have shown

they’re more willing to spend than they were at the start of the year.

The Institute for Supply Management’s gauge of factory activity in the

Midwest region fell to 55.8 in Jul from 56.8 the month prior. The forecast expected a larger decline to a reading of 54.0. Readings above 50

point to expansion, while those below indicate contraction.

The economic news was not good while earnings are coming in varied. The lack of strength in the economy makes the bulls feel better concerning extending low interest rates. But this is not the behavior expected when popular stock averages are essentially at record highs. This disconnect between economic performance & stocks prices is not new, but it still should be a cause for worry.

No comments:

Post a Comment