This blog gives investors more financial information for very smart investing!

Friday, August 28, 2015

Markets drift lower on consumer sentiment data

Dow fell 52, advancers over decliners 4-3 & NAZ slid back 1. The MLP index fund jumped another 7+ to the 362s & the REIT index fund lost 1+ to the 304s. Junk bond funds edged higher & Treasuries advanced. Oil went up to the 43s & gold saw buying.

St. Louis Federal Reserve pres James Bullard said that while

world financial markets are volatile, US fundamentals are good & the

interest rate-setting FMOC shouldn’t alter its

forecast for the economy. “The key question for the committee is -- how much would you want to

change the outlook based on the volatility that we’ve seen over the last

10 days, and I think the answer to that is going to be: not very much,”

Bullard said. “You’ve really got the same trajectory that the committee will be

looking at that we were looking at before, so why would we change

strategy, which was basically to lift off at some point,” Bullard added (he votes on the FOMC next year). If market turmoil persists, though, that could affect the timing of

the first rate increase, Bullard said later. “The committee does not like to move when there’s volatility,” he

said. “If we had the meeting this week, people would probably say let’s

wait.” He added, “but the meeting is not this week,

it’s Sept. 16 and 17.” Bullard also said he would support scheduling a

press conference following the Oct 27-28 meeting if the committee

doesn’t raise rates next month. That would make it easier for the Fed to

explain a liftoff in Oct. Fed officials are weighing when to begin raising interest rates for

the first time since 2006. While the US is growing at a solid clip,

inflation is below the Fed target & the global outlook has been

dimmed by a Chinese slowdown that is driving down commodity prices &

spurring market turbulence.

Consumer confidence declined in Aug to a 3-month low as

recent stock-market turbulence weighed on the outlook for the

US economy in the coming year. The University of Michigan consumer sentiment final index for the

month fell to 91.9 from 93.1 in Jul. The projection called for a reading of 93, little

changed from the preliminary reading of 92.9. A measure of prospects for

the economy over the next 12 months was the weakest since Nov. Confidence withered in the 2nd half of the month after stocks

plunged on concerns about the Chinese economy. A resilient labor market & cheaper fuel may nonetheless keep sentiment from slumping, which

will bolster consumer spending. The survey’s index of expectations six months from

now dropped to 83.4, the lowest since Nov, from 84.1 last month.

The initial Aug reading was 83.8. The gauge of current conditions, which

measures Americans' views of their personal finances, declined to a

three-month low of 105.1 in Aug from 107.2. The preliminary figure

was 107.1. Americans expected an inflation rate of 2.8% in the next year,

unchanged from Jul. Over the next 5-10 years, they expect a 2.7% rate of inflation, compared with 2.8% in the previous month.

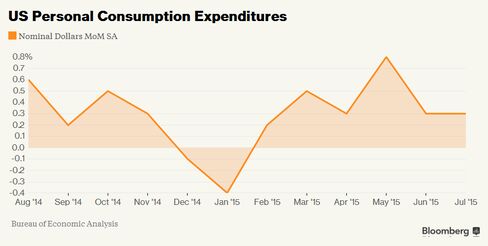

Consumer purchases climbed in Jul as incomes grew, showing the

biggest part of the US economy was off to a good start in Q3.

The

0.3% advance matched the prior month’s gain, according to the Commerce

Dept. The forecast was for a 0.4% increase.

Wages rose by the most this year. Coming on the heels of data showing spending & the overall economy

did better than previously estimated in Q2, the figures

indicate the momentum carried over into H2.

Steady hiring, cheap gasoline, rising home-equity & low borrowing

costs are underpinning demand & helping shield the U.S. from global

weakness. Total incomes rose 0.4% in Jul for a 4th month, matching

the forecast. Wages & salaries

increased 0.5%, the biggest gain since Nov. Because spending increased less than incomes, the saving rate rose to 4.9% from 4.7%. Adjusting

consumer spending for inflation, which generates the figures used to

calculate GDP, purchases rose 0.2% after being

little changed the previous month. Economic growth accelerated to a 3.7% annualized rate in Q2, revised up from a previously reported 2.3%. The 3.1% jump in

household purchases also was more than the prior estimate. Durable goods

purchases, including automobiles, jumped 1.3% after adjusting for

inflation, with about ½ the gain coming from demand for autos &

parts. That followed a 0.9% drop. Spending on non-durable goods,

which include gasoline, rose 0.1%. Household outlays on services also rose 0.1% after adjusting

for inflation. Inflation remained tame.

The price gauge based on the personal consumption expenditures index

increased 0.1% from the prior month & was up 0.3% from a

year earlier.

Stocks are taking a breather after 2 days of big gains. That was to be expected. There is also a realization that fundamental problems have not gone away. China's economy is blurry & that's being kind. The euro area is not doing well as the Greek debt mess has not been resolved. The US economy is stumbling along with in fits & starts. This week after the wild gyrations, Dow is up 150. Not bad all considered.

No comments:

Post a Comment