This blog gives investors more financial information for very smart investing!

Thursday, September 24, 2015

Markets tumble on worries about rate hike by the Fed

Dow sank 256, decliners over advancers 5-1 & NAZ lost 76. The MLP index dropped 6+ to the 312s & the REIT index fell 1+ to the 303s. Junk bond funds mixed & Treasuries rose as stocks declined. Oil went up & gold shot up (going over 1150) as stocks were sold.

The Federal Reserve held interest rates near zero last week, though

13 of 17 policy makers still expect a rise this year. That forecast

faces a major threat: The concerns that persuaded officials to delay

action are just as likely to escalate over the next 3 months as to

die down. Financial market turmoil, slower global growth &

lingering doubt about the path of inflation led the central bank to

postpone its first rate rise since 2006. Those headwinds could

abate in time for officials to lift off at their meeting in either

Oct or Dec, but should they worsen, it may kill all hope of an

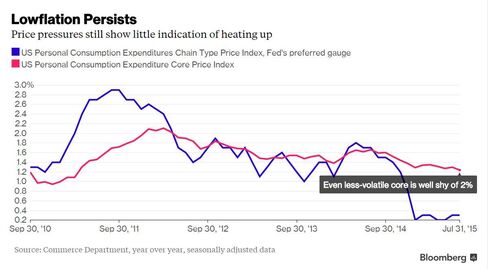

increase in 2015. Exhibit

A: There are several reasons why inflation might continue to languish

or even soften further before the end of the year, causing it to fall

short of the Fed’s already modest 0.4% 2015 estimate.

Declining

unemployment may fail to push up wages as the Fed expects because of

hidden slack in the labor market. Tumbling oil prices, while not

measured in core readings of inflation, could pass through to other

prices. And a stronger dollar could cool inflation further by dampening

the cost of imports. Though the Fed often cites the dollar &

commodity prices as headwinds that it views as transitory, they might

not be the only things contributing to subdued price pressures.

The momentum in orders for

business equipment stalled in Aug following gains the prior 2

months as. investment took a breather amid volatility in financial

markets & concerns that global growth is slowing. Bookings for

non-military capital goods excluding aircraft fell 0.2% after rising 2.1% in Jul, according to the Commerce

Dept. Orders for all durable goods, meant to last at least 3 years, dropped 2%

reflecting declines in defense & aircraft. The relatively steady

reading in capital goods bookings following the best back-to-back gains

in more than a year signals companies waiting to assess prospects for

US demand as global growth slows & financial markets turn volatile. A

strong American consumer, powered by more jobs, growing incomes & low

inflation, will be needed to help support the outlook for growth in H2. The forecast estimated

bookings for total durable goods would fall 2.3%. The Jul

reading was revised from a prior estimate showing a 2.2% gain. Shipments

of non-military capital goods excluding aircraft, which are used to

calculate GDP, decreased 0.2% after

rising 0.5% the month before. Commercial aircraft orders

dropped 5.9% after falling 8.7% a month earlier. Demand

for automobiles also took a breather, falling 1.6%. Bookings

rose 4.9% in Jul. Excluding transportation

equipment were little changed. Demand for defense

equipment dropped 24.3%, reversing the prior month’s gain. Stronger

investment in capital equipment would be a welcome boost for US

growth, which has relied on a solid pace of consumer spending this year.

Purchases of new homes jumped in Aug to a 7-year high as Americans took advantage of historically low mortgage rates. Sales climbed

5.7% to a 552K annualized pace, exceeding all forecasts & the highest since Feb 2008,

from a 522K rate in Jul that was stronger than initially reported, according to the

Commerce Dept. Steady

job gains & cheaper borrowing costs are bolstering demand for new

homes, particularly as the supply of previously owned properties is

still scant. Further healing in residential real estate should help

underpin the US economy amid weakness from the stronger dollar &

slower overseas growth. The forecast called for 515K & the Jul reading was previously reported as

507K. The median sales price increased 0.3% from Aug 2014 to $292K. Purchases

climbed in 3 of 4 US regions, led by a 24.1% jump in

the Northeast. New-home

purchases, tabulated when contracts get signed, are considered a

timelier barometer of the residential market than purchases of

previously owned dwellings.

Stocks are spooked again, another sign that this is not a healthy market. Janet will be testifying shortly & traders worry about what she might say about a rate hike. They should wake up & realize that a hike is long overdue (I remember their worries in 2013). It will probably come this year & should be a modest 25 basis points followed by a pause for at least 1-2 meetings. This much nervousness about a long overdue rate hike is a sad state of affairs for the stock market.

No comments:

Post a Comment