This blog gives investors more financial information for very smart investing!

Wednesday, December 16, 2015

Higher markets ahead on mixed economic data

Dow climbed 108, advancers over decliners an impressive 4-1 & NAZ gained 20. The MLP index added 3+ to the 253s (modest compared to recent weakness) & the REIT index went up 2+ to 320. Junk bond funds rose & Treasuries declined. Oil gave up some of its 2 day rally & gold had a strong advance.

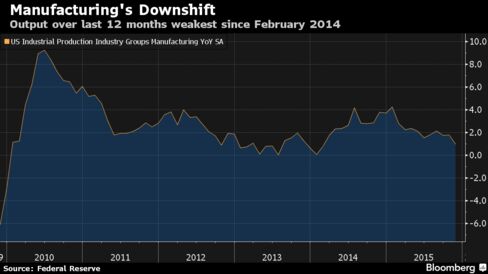

Manufacturing stagnated in Nov, held back by lower production of

durable goods such as automobiles & metals that reflects weak global

demand. The unchanged reading in factory output followed a 0.3% gain in Oct that was softer than previously reported, according to the Federal Reserve. Warmer weather led to the biggest

slump in utility output in more than 8 years, pushing down total

industrial production by the most since Mar 2012. Production has

floundered this year as dollar appreciation & weaker overseas

economies damped demand for US-made goods & as oil producers cut

back on new investment. Stronger home construction & resilient

consumer spending are making up for the malaise in manufacturing. Nov

manufacturing output, 12% of the

economy, matched the forecast. October factory production

was previously reported as a 0.4% gain. Compared with a year

earlier, manufacturing rose 0.9%, the weakest since Feb

2014.

Total

industrial production, which includes factories, mines & power

plants, dropped 0.6%, weaker than the forecast for a 0.2% decrease. Oct was revised to a 0.4% decline from a

previously reported 0.2% drop. Capacity

utilization

decreased to a 2-year low of 77% from 77.5%

the prior month. Warmer-than-usual

temps in Nov depressed utility output 4.3%, the

most since Mar 2007, after a 2.8% drop in Oct. Mining production, including oil

drilling, declined 1.1% after a 2.4% decrease.

Oil & gas well drilling dropped 4%. Factory output of

all durable goods decreased 0.2%. Motor vehicles &

parts production fell 1%, while output of primary metals

decreased 2.8%. Factory output excluding autos & parts rose 0.1%.

New-home construction in the US rebounded in Nov, led by gains

in single-family dwellings that signal the residential real estate

industry will continue to support growth. Housing

starts climbed 10.5% to a 1.17M annualized rate from a

1.06M pace in Oct, figures from the Commerce Dept. The estimate was for a 1.13M rate. Work began on the

most stand-alone houses since Jan 2008, & permits for similar

projects reached an 8-year high.

Supported

by growing payrolls & a low level of layoffs, demand for housing has

strengthened over the past year as more Americans now have the means &

the confidence to invest in a home. Building

permits, a sign of future construction, increased 11% to a 1.29M annualized rate, the most since Jun. They

were projected to rise to 1.15M. Construction of

single-family houses increased to a 768K rate from 714K in

Oct, showing gains may continue. Building applications

for single-family projects rose to a 723K pace, the most since

Dec 2007. Single-family dwellings make up the biggest part of the market and are subject to less volatility. Work

on multifamily homes rose 16.4% to

a 405K rate. 2 of 4 regions had an increase in starts in Nov, paced by an 21.3% jump in the South.

China’s central bank expects economic

growth to come in at 6.8% next year as consumer inflation

accelerates & real estate sales rebound. People’s Bank of China (PBOC) also cut the 2015 growth forecast to 6.9% from a 7% projection in Jun. Consumer prices

will rise 1.7% next year versus 1.5% this year. The report came hours after a gov-backed research institute released a forecast saying growth will slow to 6.6-6.8% next year. "We expect that the number of positive factors will gradually increase in 2016," central bank researchers wrote.

"These supportive factors include the recovery of real estate sales,

the lagged impact of macro and structural policies, as well as some

modest improvement in external demand." PBOC researchers forecast

fixed-asset investment growth would pick up to 10.8% next year

from the 10.3% increase estimated for this year. Exports are expected to increase 3.1% next

year, reversing the decline in 2015. That contrasted with the other report from the Chinese Academy of Social Sciences (CASS), which forecast a deceleration in investment & a drop in exports. CASS,

the country’s top gov-backed research organization, said in its

report the PBOC should continue to apply “structurally loose” monetary

policy. Growth

will slow from 6.9% this year to 6.5% next year & 6.3% in

2017, according to economist estimates. Last year’s 7.3% expansion was the slowest since 1990. Property investment may gradually

stabilize & recover next year, supported by rebounding land & home

sales, central bank researchers concluded. Infrastructure

investment growth may maintain a relatively rapid pace as the gov

accelerates approvals for water, rail & affordable home projects, the

staff said.

Traders are feeling good before Janet says anything. The Fed rate hike is all but guaranteed & the stock market has had plenty of time to adjust. Now it is simply a matter of finding out what Janet has to say.

No comments:

Post a Comment