This blog gives investors more financial information for very smart investing!

Tuesday, December 15, 2015

Markets rise, led by energy & financial issues

Dow jumped up 181, advancers over decliners more than 3-1 & NAZ gained 58 (going over 5K once again). The MLP index rose 1+ to the 248s (still depressed) & the REIT index added 3+ to the 317s. Junk bond funds recovered a little bit of recent losses & Treasuries dropped. Oil had a modest recovery following recent selling & gold was off a tad.

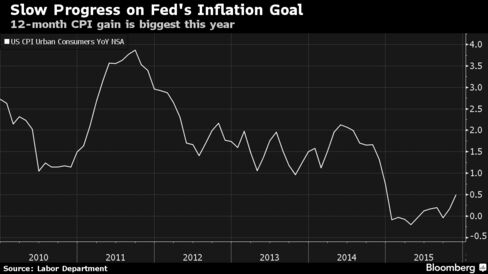

The cost of living in the US held steady in Nov, underscoring scant inflation that is well below the Federal Reserve goal. The

consumer-price index was unchanged after a 0.2% gain in Oct, according to the Labor Dept. Excluding volatile food and

fuel, the core measure rose 0.2% for a 3rd straight

month. The cheapest crude oil in years may keep inflation below the Fed 2% goal even as it

boosts Americans’ purchasing power. The CPI matched the forecast. The gauge increased 0.5% in the 12 months ended in

Nov, the most this year, after a 0.2% year-over-year

advance the prior month. The figure is expected to pick up in coming

months, reflecting easier comparisons with late last year & early in

2015, when oil prices were plunging.

The

core CPI measure increased 2% from Nov last year, the most

since May 2014, after rising 1.9% in the prior 12-month period. Energy costs decreased 1.3% from a month earlier. Food

prices fell 0.1%, driven by cheaper meat, chicken, eggs %

fish. Apparel & used vehicles also declined last month. Expenses

for shelter climbed 0.2% from a month earlier. Owners-equivalent

rent, one of the categories designed to track rental prices, also rose

0.2%. Costs of medical care climbed 0.4% after a 0.8% advance. Higher

prices for shelter, including rents & hotel rates, are helping to

prop up inflation even as oil has taken another plunge in recent weeks & the strong dollar is holding down commodity prices. Prices of all

goods decreased 2.8% in Nov from a year earlier, while the

costs of services advanced 2.5%.

Confidence among US homebuilders in Dec slipped further away

from a decade high, a sign progress in the housing industry may moderate

as developers fret over rising costs for lots & labor. The

National Association of Home Builders/Wells Fargo sentiment gauge

declined to 61 this month from 62 in Nov. Readings above 50 mean more respondents said

conditions were good. The gauge reached 65 in Oct, a 10-year high.

Momentum

in the housing market has cooled after strong gains earlier in the year

as limited wage growth has bridled how fast the industry can improve.

With the central bank considering raising its benchmark interest

rate this week, consumers & builders may hold off on

investments until the impact of higher borrowing costs becomes clearer. The forecast projected the index would increase to 63. Confidence eased in 3 of the 4 regions, with builders in the Midwest showing the greatest

decline to 55 from 60. The prospective

buyer traffic gauge dropped to 46 from 48 last month, while the current

single-family home sales index decreased to 66 from 67. The 6-month sales outlook measure fell to 67 from 69. The

confidence index is “in line with a gradual, consistent recovery,”

the NAHB said. “With job

creation, economic growth and growing household formations, we

anticipate the housing market to continue to pick up traction as we head

into 2016.”

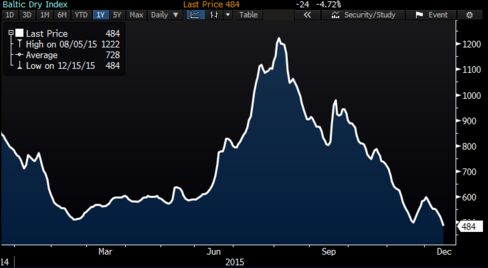

The shipping industry’s most-watched measure of rates for hauling

commodities plunged to a fresh record amid a persisting glut of ships & speculation weakening Chinese steel output could translate into

declining imports of iron ore to make the alloy. The Baltic Dry

Index fell 4.7% to 484, the lowest in Baltic Exchange data

starting in 1985. Rates for 3 of the 4 ship types

tracked by the exchange retreated. China, which makes about ½ the

world’s steel, is on track for the biggest drop in output for more than 2 decades.

Owners

are reeling as China’s combined seaborne imports of iron ore & coal, commodities that helped fuel a manufacturing boom, record the first

annual declines in at least a decade. While demand next year may be a

little better, slower-than-anticipated growth in 2015 has led to almost

perpetual disappointment for rates, after analysts’ predictions at the

end of 2014 for a rebound proved wrong. Rates for Capesize ships fell by 13-15%. The ships

are so-called because they can’t get thru the locks of the Panama

Canal & must instead sail through around South Africa or South

America. Smaller Panamaxes, which can navigate the waterway,

advanced 0.3% to $3285 a day. The two other vessel types also declined. Owners are contending

with a fleet whose capacity more than doubled over the past decade. At

the end of last year, analysts forecast rates for

Capesize-class vessels would jump by about 1/3 in 2015. By the start

of this month, they were expecting a decline of about that magnitude.

This is a bargain hunting kind of day, following all that selling last week. Until Janet tells us about interest rates tomorrow, movements don't mean much. Junk bond funds, vastly oversold, also found buyers today.

No comments:

Post a Comment