This blog gives investors more financial information for very smart investing!

Tuesday, December 22, 2015

Markets advance cautiously on mixed economic data

Dow rose 43, advancers over decliners 3-2 & NAZ went up 5. The MLP index jumped up 8 to the 271s & the REIT index added 2+ to the 322s. Junk bond funds inched higher & Treasuries retreated. Oil slid lower in the 34s & gold also sold off.

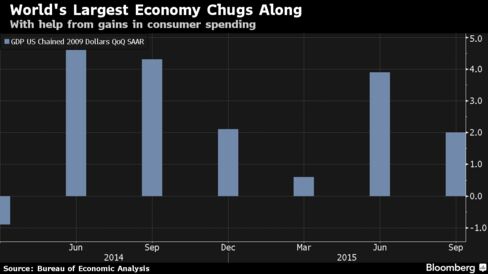

The US economy expanded at a revised 2% annualized rate in

Q3, buoyed by consumer spending as businesses struggled

to sell to overseas customers battered by sluggish growth. The

gain in GDP followed a 3.9% advance in Q2, according to the Commerce Dept. The forecast

called for a 1.9% increase compared with the previously reported

2.1% pace.

Even

with the slight reduction in growth, household purchases propelled

demand last qtr as employment improved & fuel prices remained low.

Nonetheless, consumers alone won’t be able to shoulder the burden of

helping the economy overcome slower global growth, so

areas such as business investment & gov outlays will also need

to strengthen. The economy grew at a pace of 2.3% in H1 after expanding 2.4% in all of 2014. The

slight reduction in Q3 growth reflected a smaller increase

in inventories than previously estimated. Consumer spending was little

changed from the prior report as a reduction in outlays on financial

services was offset by a bigger gain among non-profit agencies serving

households. Weaker overseas

growth & a strong dollar have weighed on net exports, with trade

subtracting 0.3 percentage point from overall growth after adding 0.2

percentage point in Q2. Sustained growth in

the combined with weakening in other parts of the globe, including

in China, could widen the gap between exports & imports going forward.

Sales of previously owned homes slumped in Nov to the lowest

level since Apr of last year as a change in industry rules lengthened

the amount of time it took buyers to close on a deal. Closings on existing homes, which usually take place a month or 2

after a contract is signed, declined 10.5% to a 4.76M

annual rate after a revised 5.32M pace in Oct, the National

Association of Realtors said. Nov sales were weaker than

the most pessimistic forecast. “November home sales without a doubt were heavily impacted by a new

federal government rule regarding closing documents,” the NAR

said,

adding that sales may rebound this month. “Buying interest is there,

it’s just that closings are not happening on a timely basis.” The forecast called for 5.35M annual rate last month. The 10.5% drop was the biggest since Jul 2010. The length of time it took buyers to close on a home purchase was 41

days, up from 36 days a year earlier. The NAR attributes that to

a change in regulation that consolidated the closing process & the

introduction of new forms that are processed by lenders and title

companies. Compared with a year earlier, purchases decreased 3.8% on a seasonally adjusted basis. Purchases of existing homes decreased in all of 4 regions. The number of existing properties on the market fell 3.3% to

2.04M, the fewest since Mar, from a month earlier.

At the current pace, it would take 5.1 months to sell those houses

compared with 4.8 months at the end of Oct. The inventory of unsold

homes was down from 2.08M a year earlier. In general, tight inventory levels have helped

boost the values of homes on the market. The median price of an existing

home rose 6.3% to $220K from Nov 2014.

Mid-Atlantic manufacturers reported an unexpected decline in factory

activity this month, reversing the improvement in Nov & providing

further indication that producers continue to struggle with weak demand & adverse currency rates. The Federal Reserve Bank of

Philadelphia said its index of general business activity tumbled to -5.9 in Dec from 1.9 a month

earlier. Readings below zero denote contraction, & the index has been

below that level in 3 of the last 4 months. Economists

expected the gauge to hang above the

expansion threshold & anticipated a reading of 1.0. Firms reported a sharp decline in new orders, sending that

subindex about 6 points lower to -9.5, while a gauge of unfilled

orders dropped to -17.7 from 2.4. Producers commanded lower prices in

Dec, pushing the prices-received subindex down to 8.7 from -0.4. Despite weaker conditions, labor market indicators improved slightly.

The index measuring the number of employees rose to 4.1 from 2.6, &

firms snapped a streak of declines in the average number of hours

employees worked. As conditions deteriorated during the month,

producers turned decidedly more pessimistic

about future prospects. The 6-month outlook gauge slid to 23.0 from

43.4, the lowest reading in about 3 years, as firms predicted

drop-offs in new orders, shipments & pricing power.

Sellers are extending their long weekend holiday, so the buyers have the upper hand today. Nothing dramatic is going on in the markets & money managers have a chance to adjust positions. Still haven't hear much about retail sales in the important holiday season. Dow remains down more than 50 YTD.

No comments:

Post a Comment