This blog gives investors more financial information for very smart investing!

Thursday, October 20, 2016

Lower markets as oil drops below $51 and on earnings

Dow gave back 56, decliners over advancers 5-2 & NAZ fell 22. The MLP index fell 2+ to the 312s & the REIT index was flat in the 344s. Junk bond funds were mixed & Treasuries crawled higher. Oil dropped 2% & gold continued climbing higher.

China's holdings of US Treasuries fell to the lowest level since

Nov 2012, as the it draws down its

foreign reserves to prop up the yuan. The biggest foreign holder

of gov debt had $1.19T in bonds, notes & bills in

Aug, down $33.7B from the prior month, the biggest drop since

2013, according to the Treasury Dept. The

portfolio of Japan, the 2nd largest holder, fell for the first

time in 3 months, down $10.6B to $1.14T. Saudi

Arabia's holdings declined for a 7th straight month,

to $93B. China sold

an estimated $570B in foreign-exchange assets from Aug 2015 to

Aug 2016 in an effort to keep the currency from plunging, according

to an estimate by the US Treasury. It reiterated that China's

efforts to support the yuan were preventing a rapid depreciation that

would hurt the global economy. China's foreign-exchange reserves

fell $16B to $3.19T in Aug & are down from a peak

of close to $4T in 2014. The reserves dropped another $19B in Sep to the lowest level since 2011. The

report also showed

net foreign buying of long-term securities totaling $48.3B in

Aug. Total cross-border inflow, including short-term

securities such as Treasury bills & stock swaps were $73.8B. Net

foreign selling of US Treasuries was $24.8B in Aug, while

foreigners purchased a net $2.73B in equities, $22.8B of

corp debt & $29.6B in agency debt.

The ECB kept its quantitative-easing program &

interest rates unchanged as suspense builds up over a possible extension

of bond-buying later this year. The Governing Council

left the main refinancing rate at zero, the deposit rate at minus 0.4% & asset purchases at €80B ($88B) a month,

as predicted. “The Governing Council continues to expect the key ECB interest rates

to remain at present or lower levels for an extended period of time,

and well past the horizon of the net asset purchases,” the ECB said. “The Governing Council confirms that the monthly asset

purchases of 80 billion euros are intended to run until the end of March

2017, or beyond, if necessary, and in any case until it sees a

sustained adjustment in the path of inflation consistent with its

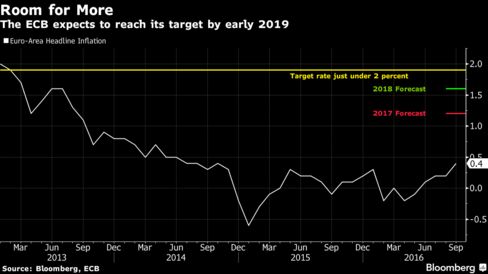

inflation aim.” Draghi has

expressed confidence inflation will return to the ECB's goal of just

below 2% by early 2019 at the latest & the majority view of

economists is that he will eventually extend QE to

reach that goal.

The

ECB's position so far has been that QE will run until Mar “or beyond,

if necessary.” That the program has enough flexibility to secure a

sustained return to the inflation target. Price growth, currently at

0.4%, is only slowly picking up.

Sales of previously owned US homes increased more than projected in

Sep, showing residential real estate continues to contribute

modestly to growth, National Association of Realtors data showed. Contract closings rose 3.2% to a 5.47M annual rate (forecast was 5.35M). Sales climbed 2.8% from Sep 2015 before seasonal adjustment. Median sales price increased 5.6% from Sep 2015 to $234K. The inventory of available properties dropped 6.8% from a year earlier to 2.04M. Solid job growth, a recovery in home values since the last recession &

30-year fixed mortgage rates near the lowest level since the 1970s are

keeping residential real estate on a steady path forward. At the same

time, home prices continue to outpace income gains, limiting the

strength of housing & the market’s impact on economic growth. A pickup

in construction would give Americans more homes to choose from,

boosting turnover & helping bring about more moderate price gains

needed to attract a larger share of first-time buyers. Property listings

declined on a year-over-year basis for a 16th consecutive month in

Sep.

Earnings are not inspiring a lot of confidence in the stock market. Oil is a commodity subject to wild fluctuations. Asking a group of countries with different agendas to agree on anything is always difficult. Setting guidelines for lower production is no different. Meanwhile sluggish growth of the US economy is a dark cloud for stocks & that is not going away.

No comments:

Post a Comment