This blog gives investors more financial information for very smart investing!

Thursday, October 27, 2016

Mixed markets on mixed economic data

Dow slid back 11, decliners over advancers 2-1 & NAZ fell 13. The MLP index lost 2 to the 307s & the REIT index sank 6+ to 332. Junk bond funds were mixed & Treasuries were sold, taking the yield on the 10 year Treasury up towards 1.9%. Oil rose (but still under 50) & gold inched higher.

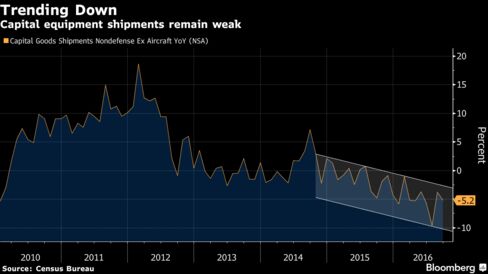

Orders for US business equipment fell in Sep by the most in 7 months, indicating corp investment is having trouble gaining

traction. Bookings for non-military capital goods excluding

aircraft dropped 1.2%, erasing a 1.2% Aug gain that was

stronger than previously reported, according to the Commerce Dept. The forecast called

for a 0.1% drop. Demand for all durable goods eased 0.1%. Business

investment remained slow in Q3 as moderating demand and

weakness overseas prompted companies to hold back. Even with stability

in the oil sector, an inventory correction & growth in consumer

spending, manufacturing will probably see little more than a gradual

improvement. Orders declined for fabricated & primary metals, computers & electronics, & communications equipment. The

drop in bookings for all durable goods last month followed a 0.3% Aug advance that was better than previously reported. Orders

for non-defense capital goods excluding aircraft are a proxy for future

business investment in items like computers, engines & communications

gear. Even with the decline, bookings over the 3 months ended in

Sep rose at a 5.2% annualized pace, indicating the worst of

the investment slump is over. Nonetheless,

shipments of those goods, which are used in calculating GDP, fell an annualized 4.4% in Q3. They were up 0.3% from a month earlier after little

change in Aug. Compared with a year earlier, sales of capital

equipment were down 5.2%.

Durable goods orders excluding

transportation equipment, which are often volatile from month to month,

climbed 0.2% after a 0.1% gain.

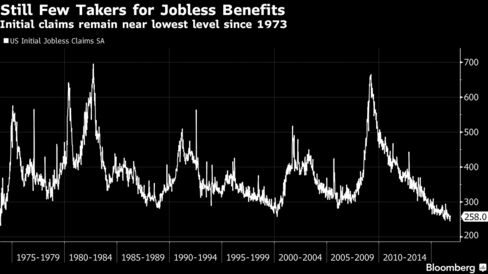

Filings for US jobless benefits fell for the first time in 3

weeks, staying near a 4-decade low as employers remain unwilling to

part with workers. Jobless claims declined 3K to 258, according to the Labor Dept. The forecast called for

256K. Continuing claims dropped to the lowest level since 2000.

With

the job market improving & the unemployment rate holding at or below 5% this year, fewer skilled candidates are available for openings,

prompting managers to hold onto their staffers. Filings have been below

300K for 86 straight weeks, the longest streak since 1970 & a

level typical for a healthy labor market. The 4-week average of claims increased to 253K from

252K in the prior week. The number continuing to

receive jobless benefits dropped 15K to 2.04M & the unemployment rate among people eligible for benefits

held at 1.5%.

Contracts to buy previously owned US homes rose more than expected

in Sep, another sign of the underlying momentum in the housing

market. The National Association of Realtors (NAR) pending

home sales index, based on contracts signed last month, increased 1.5% to 110.0 following a drop in Aug. The index was 2.4% higher than in Sep 2015. The forecast was for pending home sales to rise 1.2%. The pending home sales index for

Aug was revised slightly lower to 108.4. Across the nation's 4 regions, contracts jumped 4.7% in

the West & also rose in the South. They fell 1.6% in the

Northeast & edged down in the Midwest. Separate data last week showed that home resales surged in

Sep after 2 straight months of declines as first-time buyers

stepped into the market.

Not much going on today. Less than satisfactory earnings reports are dominating the news & the bulls are not able to take stocks higher. The Dow chart below says it all, going nowhere fast. Tomorrow the first estimate for Q3 GDP will be reported & that should be unexciting.

No comments:

Post a Comment