This blog gives investors more financial information for very smart investing!

Wednesday, October 19, 2016

Mixed markets on Fed outlook & earnings

Dow gained 27, advancers over decliners about 3-2 & NAZ lost 5. The MLP index added 1 to the 314s & the REIT index was off 1+ to 342. Junk bond funds were a little higher & Treasuries were flattish (more below). Oil jumped up, going over 51, & gold rose.

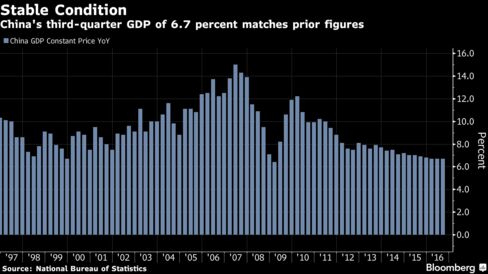

China’s economic growth remained stable in Q3, all but

ensuring the gov's full-year growth target is met & opening a

window for policy makers to deliver on vows to rein in excessive credit & surging property prices. GDP rose 6.7% from a year earlier, matching the

projection & in the middle

of the gov 2016 goal of 6.5-7% growth.

Services industries paced the expansion in the first 9 months of the

year, expanding 7.6%.

Stabilizing growth gives room for policies aimed at containing swelling leverage & curbing excessive financial risks, with IMF nresearchers among those calling for such efforts. The gov released guidelines last week for reducing debt, yet past pledges have often been ignored

as rampant credit growth fuels surging house prices in its

biggest cities. Releases

for Sep showed the continuing shift in China's economy toward

consumer spending, with retail sales gains outpacing the rise in

industrial production. Investment spending continues to be led by the

public sector, with subdued private business

spending highlighting the problem of high levels of debt.

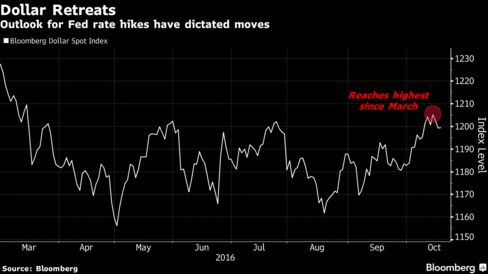

The $ fell for a 3rd day after a core US

inflation gauge rose less than forecast in Sep suggesting the

pace of interest-rate increases by the Fed will be gradual. The currency dropped as the chances of a Fed rate hike by Dec, according to fed

fund futures pricing, receded amid mixed signals from the economy.

Traders see about a 64%

probability the central bank will raise rates by Dec, down from 66% at the end of last week. The calculations assume that the

effective fed funds rate will average 0.625% after the next

increase. The ECB is due to announce its decision on monetary

policy tomorrow. Economists expect

that officials will keep the deposit rate at a record-low minus 0.4%. There has been speculation that the ECB will began to reduce

its bond purchases next year, following a report earlier this

month that policy makers led by pres Mario Draghi had discussed

tapering.

Homebuilders pulled back on construction for a 2nd straight month

in Sep, with a plunge in apartments offsetting gains in

single-family homes. Building activity was weak in all parts of the

country except the Midwest. The Commerce Dept says construction tumbled 9% in

Sep to a seasonally adjusted annual rate of 1.05M units, the slowest pace in 18 months. Construction had fallen 5.6%

in Aug. The weakness last month reflected a 38% drop in

construction of apartments, which overshadowed an 8.1% rise in

single-family construction. Despite the 2 months of declines, home construction has been

one of the bright spots in the economy this year with builders

scrambling to keep up with rising demand, reflecting continued strong

job gains.

On mixed messages, stocks are looking for direction. In the Sep-Oct period, Dow has had a flat performance. Buyers have been encouraged by what they see as prospects of postponing the next rates hike at the Fed while economic data is inconsistent & drab.

No comments:

Post a Comment