Dow vaulted 394 closing at the highs, advancers over decliners 7-1 & NAZ climbed 107. The MLP index rose 2 to the 254s & the REIT index gained 6 to the 312s. Junk bond funds were higher & Treasuries rallied, taking the yield on the 10 year bond down to 2.93%. Oil had a good advance but below the AM highs & gold edged higher.

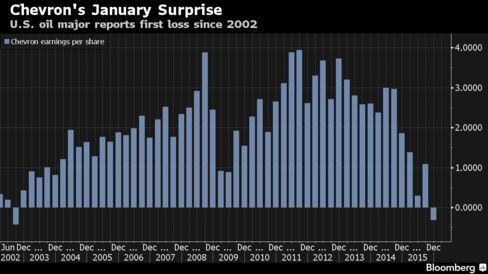

Chevron, a Dow stock, is the first super-major oil producer to report

Q4 results, & posted its first loss since 2002. It's bracing for a review of its credit rating. A glut of crude

from the Persian Gulf and North American shale fields has collapsed

prices, forcing the company to write down the value of its

fields. Despite the red ink, CVX still plans to pay $2B in divs in about 6 weeks to fulfill a

promise to protect payouts at all costs. The company

probably will cut spending on new projects for a 4th consecutive

year in 2017 to as little as ½ the $42B it spent in 2013. The Q4 net loss was 31¢ per share, compared EPS of $1.85 a year earlier. The loss was

worse than any analyst predicted.

Earnings were hurt

by $1.1B in charges as the plunge in energy prices slashed the

long-term earning power of its portfolio of oil & gas holdings. The impact of tumbling prices more than

wiped out any upside from the 3.5% increase in output from it wells & its geologists discovered

enough new crude & gas to replace 107% of what it produced

during 2015. The stock rose 55¢. If you would like to learn more about CVX, click on this link: club.ino.com/trend/analysis/stock/CVX?a_aid=CD3289&a_bid=6ae5b6f7

For the first time in almost a decade, China has lost ground in

catching up with the US economy, when output is measured in dollars. US

GDP increased $590B in 2015 from a year

earlier. China's economy, while

reporting 6.9% growth for the year, added $439B, as a

weaker yuan sapped the value of output gains in dollar terms.

Last

year was the first time since 2006 that China made no progress in

closing the gap with the world's largest economy. While the US economy

expanded 2.4% for a 2nd straight year, China slowed to the weakest expansion pace in a qtr-century as old growth drivers like heavy industry & exports slow. As

for 2016, China's economy is forecast to expand 6.5% in real

terms, while the yuan is projected to depreciate to 6.79 against the $, down more than 7% from the average level in 2015.

Business activity across the Midwest rebounded in Jan as producers

saw a sharp increase in orders, adding to hopes that the US economy

claws back in Q1 after an anemic end to last year. The Chicago Business Barometer, also known as the Chicago PMI, jumped

to 55.6 from 42.9 in Dec, marking the best clip of growth in a

year. Readings above 50 represent expansion. Economists anticipated a much smaller improvement to 46.0.

A surge in new orders boosted activity in the region, with a gauge of

new business rising more than 20 points to 58.8, the best in 12 months.

Production, meanwhile, moved back to positive territory. Though the report was much stronger than expected, Philip Uglow, chief

economist of MNI Indicators, the compiler of the report, expressed

caution. "Previously, surges of such magnitude have not been maintained

so we would expect to see some easing in February," he said. "Still, even if activity does moderate somewhat next month," he added,

"the latest increase supports the view that GDP will bounce back in Q1

following the expected slowdown in Q4."

The Bank of Japan unexpectedly adopted a negative interest rate policy today which brought out buyers for stocks. The economy has been troubled, but it may take more than this move for a cure. Meanwhile, the US economy is having a difficult time advancing, demonstrated by disappointing GDP data. Following today's rise, Dow is still down almost 1K in Jan making for one ugly month. Treasuries are attracting buyers with the yield on the 10 year bond at the lowest since May (negative bets on the stock market). The strength of today's rally without fundamental support is a big worry!!

Dow gained 175, advancers over decliners almost 6-1 & NAZ advanced 32. The MLP index rose 7+ to 260 & the REIT index added 1+ to 308. Junk bond funds climbed higher & Treasuries also are being up. Oil shot up to the 34s & gold is flattish in the low 1100s.

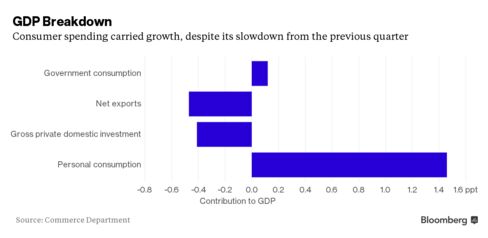

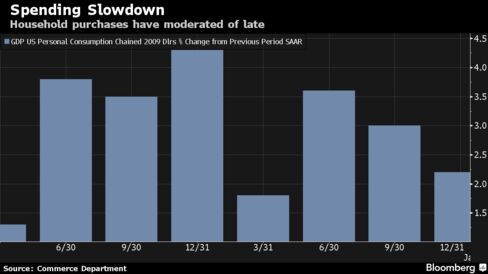

The US economy expanded at a slower pace in Q4 as

households tempered spending & businesses cut back on capital

investment & adjusted inventories. GDP rose

at a 0.7% annualized rate

after a 2% gain in Q3, according to the Commerce Dept. The advance was in line with the

forecast of 0.8%.

Growth

has downshifted as producers contend with slowing markets abroad, the

negative effect on exports from a stronger $ & plunging oil

prices that have caused drilling firms to retrench. Consumers, enjoying

the fruits of a robust labor market and cheaper fuel bills, will have to

pick up the slack if growth is expected to get back on track. GDP

expanded 2.4% for a 2nd straight year, led by the biggest

gain in consumer spending in a decade. The economy got off to a rocky

start in 2015, partly due to bad winter weather & a West Coast port

workers dispute, before rebounding in Q2. Growth moderated in the ensuing months as companies worked down bloated stockpiles & continued to battle weak exports markets. Household purchases rose at a 2.2% annualized pace

in Q4, compared with a 3% rate in the previous

period. Personal consumption added 1.46 percentage points to growth.

Final

sales to domestic purchasers, or GDP excluding trade & inventories,

climbed at an inflation-adjusted 1.6% annualized rate, compared with a 2.9% pace in the previous 3

months. A pickup in household purchases

will be needed to help the economy fight through the negative effects of

the global slowdown & the rout in commodities that’s diminishing

investment. While businesses are struggling, American households

have plenty of ammunition to assist the economy. Consumer confidence

levels have held in, powered by solid gains in the job market & low

inflation.

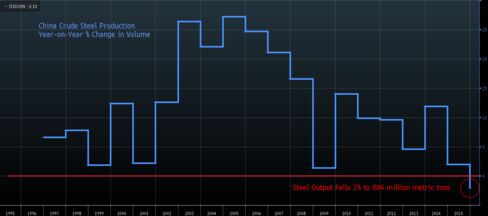

Steel

mills in China reported their first annual decline in output since 1981

as local demand contracted, prices sank to a record low & producers

struggled with overcapacity. The China Iron & Steel Association said

crude steel output shrank 2.3% to 803.8M metric tons. In

recent years China has churned out about ½ the world's steel.

Consumer sentiment of the US economy dipped this month, a sign that

global turmoil may be starting to wear on American consumers.

The University of Michigan's final consumer index for Jan fell to 92 from 93.3 recorded earlier this month. The final

Jan result was a decrease from Dec, when the index hit 92.6. Analysts had expected a reading of 93.

Stocks are being big higher to close out a very drab month. After today's rise, the Dow is still down a massive 1.2K in Jan. Economic data keeps coming in glum while oil is well off its recent lows in the mid 20s. Treasuries rose today, indicating this rally may have more to do with traders evening out month end positions.

![Live 24 hours gold chart [Kitco Inc.]](http://www.kitco.com/images/live/gold.gif?0.13539662843496858)