This blog gives investors more financial information for very smart investing!

Wednesday, January 6, 2016

Market losses in 2016 continue as oil sinks below $34

Dow tumbled 252 (but off the lows), decliners over advancers 3-1 & NAZ fell 55. The MLP index plunged 14+ to the 278s (also off the lows) as oil hit new lows & the REIT index lost 1+ to the 325s (although it has been flattish in recent months while other high yield securities were being sold). Junk bond funds puled back & Treasuries rallied. Oil tumbled to the 33s, another multi year low, & gold rose with growing uncertainty in global financial markets.

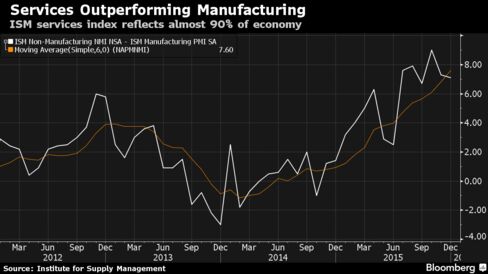

American service companies continued to outperform their

manufacturing counterparts in Dec as orders & employment picked

up, indicating the economy will keep expanding this

year. The Institute for Supply Management non-manufacturing

index, which covers almost 90% of the economy, came in at 55.3

last month, with readings greater than 50 signaling growth. While the

level is down from 55.9 in Nov & the weakest since Apr 2014, the

drop was caused by a plunge in the deliveries component that indicates

suppliers had fewer order backlogs to process. The gap between the

ISM services & manufacturing gauges has

averaged almost 8 points over the past 6 months, the widest over a

similar period since 2001. The disparity signals retail, construction & health care are among the industries less affected by the slowdown

in global demand & surge in the value of the dollar that have hurt

factories.

The forecast called for a Dec reading of 56. The measure averaged 57.1 in 2015, up

from 56.3 in the previous year & the best annual performance in a

decade. The US reading was at odds with other services measures overseas. A private Chinese services gauge slumped to its 2nd-lowest reading since the series began a decade

ago, according to Caixin Media & Markit Economics. Confidence among UK service firms dropped to a 3-year low last month, Markit Economics data also showed. On a more positive note, a combined manufacturing & services gauge in the euro area unexpectedly rose to

54.3 in Dec from 54.2 the prior month, the London-based Purchasing

Managers’ Index said. The

ISM new orders gauge in the US climbed in Dec to 58.2 from 57.5

the prior month, while a measure of services employment increased to

55.7 from 55. The business activity index, which parallels the

ISM factory production gauge, advanced to 58.7 from 58.2 in

Nov. A measure of prices paid declined to 49.7, indicating costs

were easing, from 50.3.

The US trade deficit narrowed in Nov likely as efforts by

businesses to reduce an inventory overhang pushed imports of goods to

their lowest level in nearly 5 years, outpacing a drop in exports. The Commerce Dept said the trade gap fell 5.0% to $42.4B. The trade deficit in Oct was revised up to

$44.6B from the previously reported $43.9B. Despite the shrinking trade deficit, declining exports are the latest

indication that economic growth braked sharply in Q4.

While inventories likely accounted for much of the drop in imports, the

weakness could also be pointing to a slowdown in domestic demand, which

was flagged by weak Dec automobile sales. Economists had forecast the trade gap widening to

$44.0B. When adjusted for inflation, the deficit fell

to $59.60B from $61.03B in Oct. Trade, which subtracted 0.26 percentage point from GDP in Q3, is likely to have remained a drag on

growth in Q4. A strong dollar & the inventory bloat, which has left businesses

with little appetite to order more merchandise, have combined with

spending cuts in the energy sector to take some steam out of the economy

in recent months. Economists this week slashed Q4 GDP growth

estimates by as much as one percentage point to as low as a 0.5%

annual pace, which also accounted for unseasonably warm weather that has

impacted on sales of winter apparel & other merchandise. The economy grew at a 2% annual rate in Q3. Businesses accumulated a record pile of inventory in H1-2015, which was unmatched by demand, leaving warehouses bulging with

unsold goods. Imports of goods dropped 2.0% to $183.5B,

the lowest level since Feb 2011. Imports of industrial supplies &

materials were the weakest since May 2009. There were also declines in

imports of capital & consumer goods. Auto imports, however, rose. Lower oil prices as well as increased domestic energy production also

helped to curb the import bill. The price of petroleum averaged $39.24

per barrel in Nov, the lowest level since Feb 2009 & down from $40.12 in Oct & $82.92 in Nov 2014. The $ gained almost 10% last year, eroding the appeal of

US-made goods overseas. Lackluster global demand also has put a damper

on exports. Goods exports slipped 1.1% to $122.2B, the lowest since Jun 2011. Exports of industrial supplies & materials hit their lowest level

in 5 years, while petroleum exports were the weakest since Dec

2010. Exports of non-petroleum products dropped to their lowest level

since Jun 2011. The decline in exports to the US main trading partners

was nearly broad-based, but the politically sensitive

US-China trade deficit fell 5.2% to $31.3B in Nov.

The FOMC unanimously agreed that the US

economy was ready for a rate hike in Dec but opinions are still

varied as to the trajectory of further increases as inflation remains a

wild card, minutes from the Fed Dec meeting show. The policy-setting committee voted 12-0 to raise

the short-term fed funds rate by 0.25% off the near-zero range where

rates had been held since late 2008 as FOMC members coalesced around

growing confidence that strengthening labor markets will help the US

absorb higher borrowing costs. “Members agreed that a range of recent labor market indicators,

including ongoing job gains and declining unemployment, showed further

improvement and confirmed that underutilization of labor resources had

diminished appreciably since early this year,” the minutes state. The rate of inflation growth going forward, among other economic

indicators, will dictate the future path of interest rates & FOMC

members have differing opinions on what that trajectory will be. According to the minutes, “… some members said that their decision

to raise the target range was a close call, particularly given the

uncertainty about inflation dynamics, and emphasized the need to monitor

the progress of inflation closely.” Most analysts expect 2 (possibly 3) more 0.25% rate hikes in

2016 but that will depend on continued momentum particularly in labor markets. Fed policy makers are looking especially at wage growth which was

weak throughout 2015 but is now showing signs of meaningful growth. If

wages rise in combination with strong job creation, that should push

inflation upward toward 2%. At least that’s what influential FOMC members are betting on. “Nearly all (FOMC members) continued to anticipate that inflation

would rise to or very close to 2 percent over the medium term as the

transitory effects of declines in energy and import prices dissipated

and the labor market strengthened further,” the minutes said. Yet the minutes show that “some members” remain wary of their current

inflation forecasts. Risks include additional downward pressure on

energy prices & a higher dollar valuation, which “could delay or

diminish the expected upturn in inflation.”

With the losses so far this week, it is almost certain that first week of the new year will be a down week. Some follow that as a forecaster for all of the new year. The bear market in oil, & this is one of its worst bear markets in history, is damaging numerous economies. The expected rise in US interest rates is especially painful in the stock market after so many for so long have gotten spoiled with low interest rates. There is one bright spot. In the high yield arena, REITs have held up fairly well with the index near where it was last May. Not bad with all the selling elsewhere. Dow is down more than 500 this week, under 17K & heading south.

![Live 24 hours gold chart [Kitco Inc.]](http://www.kitco.com/images/live/gold.gif?0.8023091330235299)

No comments:

Post a Comment