This blog gives investors more financial information for very smart investing!

Tuesday, January 5, 2016

Markets fluctuate after yesterday's sell-off

Dow gave 10, advancers ahead of decliners 4-3 & NAZ went up 8. The MLP index fell 2+ to the 289s & the REIT index added 3+ to the 323s. Junk bond funds were a little higher & Treasuries were sold. Oil is heading lower& gold was flattish.

Fiat Chrysler (FCAU) US sales rose 13% on

the back of gains for Jeep sport utility vehicles, as carmakers report

monthly results expected to topple the annual American sales record set

15 years ago. Nissan did better than expected, while Ford (F), GM

(GM) & Toyota (TM) missed estimates. FCAU sales reached 217K

cars & light trucks, for a 69th straight monthly gain. While a record total for the

month, that increase fell short of the 19% average estimate. Jeep deliveries increased 42% from a year earlier, led by the Cherokee & Grand

Cherokee.

Americans

renewed love of pickups & SUVs, spurred by low gasoline prices, cheap

credit, rising discounts & a strengthening labor market, boosted

demand for Jeep’s growing lineup. Full-year Jeep sales rose 25% to 865K. Nissan, which reported a 19% jump

that beat the 16% estimate. The biggest automakers were all expected to report gains of at least 10%, but

Ford & GM missed the mark. Ford light-vehicle sales rose

8.3%, compared with the 11% estimate, while GM grew 5.7%, missing the 10% forecast.

TM. sales rose 11%, just shy of the 12%

average. Industrywide

sales are expected to exceed an 18M sales rate for a record 4th straight month, helping make 2015 the best year ever for

automakers. FCAU projected an 18.3M pace, including medium & heavy-duty

trucks, which typically account for at least 200K sales. For the industry, 2015 record results would mark a 6th straight year of growing US sales, the longest streak since World War II. The surge is owed in part to buyers who were

soothed by job & wage growth, falling gasoline prices & carmakers

who upgraded their lineups & used discounts & cut-rate financing to

draw shoppers to showrooms.

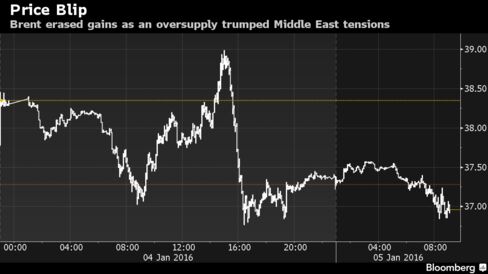

At almost any other time, an escalating diplomatic conflict between

OPEC members Iran & Saudi Arabia would mean a spike in oil prices. That

the rally this time couldn't be sustained shows just how abnormal

things are in the oil market. Brent crude is little changed this week as

a global supply glut & the slowest Chinese growth in a generation

trumped mounting strife between the nations on either side of the

world's busiest waterway for oil tankers.

There

was little more than a blip in crude futures when Saudi Arabia severed

diplomatic ties with Iran, as investors focused instead on record stockpiles & rising supply.

As Kuwait & the UAE lined up to support Riyadh, the

internal divisions that prevented OPEC from making production cuts even as prices plunged

to an 11-year low appeared more entrenched than ever. Saudi

Arabia gave Iran’s ambassador 48 hours to leave after protesters set

its embassy in Tehran on fire following the execution of a Saudi cleric, a critic of the kingdom’s treatment of its Shiite minority. It was the worst clash between the nations since the 1980s, adding to proxy wars they were

already fighting from Syria to Yemen in a quest to gain influence in the

MidEast.

China struggled to shore up shaky sentiment after

its stock indices & yuan currency tumbled, rattling markets worldwide,

but analysts warned investors to buckle up for more wild price swings

in the months ahead. Both the central bank & the stock regulator reacted quickly, & major indices recouped most of their initial early losses Tues despite a late

afternoon scare. The People's Bank of China (PBOC) poured nearly $20B into

money markets, its largest cash injection since Sep, & traders

suspected it was using state banks to prop up the yuan at the same time. The China Securities Regulatory Commission (CSRC) announced it was planning new rules to further restrict share sales by

major stakeholders in listed companies & said it would further tweak

the circuit breaker mechanism amid criticism that it had fueled the Mon

sell-off. The blue-chip CSI300 index ended up 0.3% at 3478

after bouncing in a 4% range, while the Shanghai Composite Index

dipped 0.3% to 3287. How long any reprieve will last is still in question. Keeping China's notoriously volatile and speculative stock markets

stable will be a trick. Some market watchers say the gov

interventions have kept stock valuations excessively high given the

cooling economy & falling profits.

The Chinese & American stock markets have settled down after a wild day yesterday. These are not bullish times. Economies around the world are sputtering, not turning in positive numbers. Then there is political chaos highlighted by growing tensions in the MidEast. The Dec jobs report will be announced on Fri & that should have similar data to recent monthly employment reports. Jan is shaping up as a tough month for the stock market.

No comments:

Post a Comment