This blog gives investors more financial information for very smart investing!

Thursday, January 21, 2016

Rising markets led by slightly higher oil prices

Dow bounced back 93, advancers over decliners 2-1 & NAZ went up 29. The MLP index recovered 1+ to the 214s (but down a massive 340 from the record highs in 2014) & the REIT index was off fractionally to the 298s. Junk bond funds slid lower & Treasuries rose. Oil rebounded (if you can call it that) slightly in the 26s & gold fell below 1100.

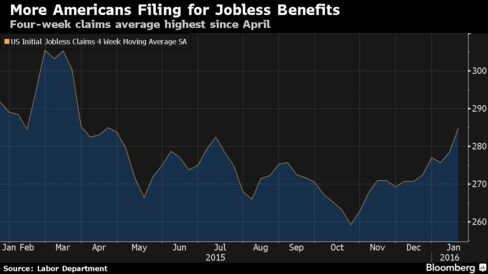

The number of applications for unemployment benefits unexpectedly

increased last week to a 6-month high, indicating tempered progress in

the labor market. Initial jobless claims climbed 10K to

293K, according to the Labor Dept. Last week coincided with the period that the

gov surveys businesses & households to calculate payrolls and

the jobless rate for Jan. Plunging oil prices may encourage

further cuts in the energy sector at the same time manufacturers

reconsider headcounts as the global economy slows. Even so, a sustained

rise in jobless claims would be needed to confirm that layoffs are on

the rise & suggest a general weakening in the labor market. Applications last week were the most since Jul 4. The forecast in a called for claims of 278K. The 4-week moving

average increased to

285K, the highest since mid-Apr, from 278K. That compares with

an average of 270K during the comparable employment survey period for

Dec.

Even

with the unexpected increase, claims have held below 300K since

early Mar, a level that is typically consistent

with an improving job market. The number continuing

to receive jobless benefits fell 56K,

the most since early Jul, to 2.21M. The unemployment rate among

people eligible for benefits dropped to 1.6% from 1.7%.

China's central bank cranked up cash injections in its money-market

operations for the 3rd week in a row, heading off a squeeze as a

seasonal jump in demand for funds coincides with surging capital

outflows. The People's Bank of China added 400B yuan ($61B) to the financial system using reverse-repurchase agreements,

the most in 3 years, bringing net injections via its various lending

tools for the month to more than 1T yuan. The Chinese New Year

holiday, a period when families get together for celebrations &

exchange gifts, will shut banks for the week starting Feb 8. China is trying to hold

borrowing costs down to support its economy without spurring a capital

exodus that drove the yuan to a 5-year low this month. GDP rose last year at the slowest pace in a qtr century &

intervention to prop up the exchange rate led to a record $513B

drop in the nation’s foreign-exchange reserves. The

PBOC conducted 110B yuan of 7-day reverse-repos & 290B yuan of 28-day contracts, more than the 160B yuan that

matured. It also injected 762.5B yuan into the banking system via 3-, 6- & 12-month loans, while Short-Term Liquidity Operations were used to add 55B yuan of 3-day loans on Mon & a further 150B yuan

of 6-day funds on Wed. In addition, the monetary authority

auctioned 80B yuan of 9-month treasury deposits to ensure liquidity supply. An

estimated $843B of capital flowed out of China in the 11 months

thru Nov & policy makers

are having to add funds to the financial system to prevent interest

rates rising as money exits.

Mario Draghi said the ECB may bolster stimulus in

Mar as threats to the euro-area recovery mount. The single currency

slid. “Downside risks have increased again amid heightened

uncertainties about emerging-market growth prospects,” he said after officials kept interest

rates unchanged at record lows. “The credibility of the ECB would be

harmed if we weren’t ready to revise the monetary-policy stance.” The ECB risks seeing its inflation-boosting package of negative

interest rates & at least €1.5T ($1.6T) in bond

purchases thwarted by a Chinese economic slowdown that threatens to cool

global growth. Emphasizing the central bank's commitment to its

ultra-loose policy settings, Draghi began his statement by reverting to

forward-guidance language & declaring that interest rates will “remain

at present or lower levels for an extended period of time.” The

ECB kept its deposit rate at minus 0.3% & the main refinancing

rate at 0.05%. A

chief concern for policy makers is that slumping oil & intl

financial-market turmoil is weighing on consumer prices.

Brent

crude has dropped almost 40% since the ECB Dec 3 meeting,

when policy makers cut the deposit rate & extended their bond-buying

program until at least Mar 2017. Euro-area inflation was 0.2%

last month, still far below the central bank goal of just under 2. Inflation expectations as measured by 5 year, 5 year

forwards are slumping.

There was buying in the PM yesterday in a VASTLY oversold market. At its lows, Dow was down an ENORMOUS 2K in Jan. Even beaten up high yield securities found buyers. All considered, today's rise in stocks is mostly bargain hunting in an extremely oversold stock market. Market breadth is meager & it is becoming more certain that Jan will be a down month for the stock market. China pumping mopney into the economy may have negative consequences later in 2016. US GDP estimates for Q1 are being revised lower & 2016 has the makings of glum year.

No comments:

Post a Comment