This blog gives investors more financial information for very smart investing!

Tuesday, November 15, 2016

Lower Dow after 6 days of gains

Dow fell 34, advancers over decliners almost 2-1 & NAZ recovered 38. The MLP index shot up 4+ to the 303s & the REIT index added 1+ to the 328s. Junk bond funds finally found buyers & Treasuries are now only about even (more below). Oil was up to the 45s & gold edged higher.

The fallout from Trump's election eased

off in financial markets with Treasuries & emerging markets halting

their routs. Oil surged. Treasury 10-year note yields fell from

this year's high & Italian bonds led gains in the euro area,

outperforming German bunds, which investors tend to favor in times of

turmoil. Shares in developing nations advanced after the biggest slide

since Aug, while US stocks fluctuated. The $ erased losses

after data showed US retail sales beat estimates. Crude jumped as OPEC

nations were said to be making a final diplomatic effort toward

securing a deal to curb production and stabilize prices. Copper tumbled.

Trump's

victory, which came with pledges to cut taxes, spend more than

$500B on infrastructure & restrict imports, triggered a record

selloff in global bonds as traders assessed the implication for

inflation & interest rates. Some have already expressed skepticism that Trump's proposals will be fully backed by Congress. The

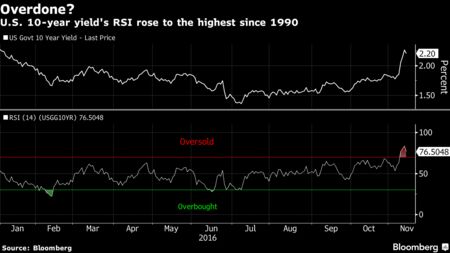

yield on benchmark Treasury 10-year notes dropped 3 basis points to 2.23%. The 41 basis-point jump over the last 3 trading sessions marked the

steepest climb in more than 7 years & the 14-day relative

strength index for the securities indicated they were the most oversold

since 1990, a potential signal that they may be set for a reversal.

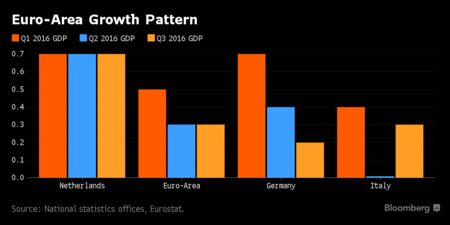

German economic growth slowed to the weakest pace in a year last

qtr, a reminder of the fragility of the euro area's recovery in a

time of rising uncertainty. The slowdown in Germany to 0.2%, along with a resumption of growth in Italy & France, left

expansion in currency region at 0.3%, in line with

an initial estimate & matching the pace of Q2.

Germany's fortunes are key to the recovery of

the euro region, where the economy’s expansion is stuck at mediocre

levels. That backdrop will color the ECB's review of

its stimulus program in less than 4 weeks, when it will also have to

factor in a global outlook characterized by the rise of populists

critical of international trade deals. Economists forecast that the euro area will maintain

its current pace of growth thru H1-2017, then see a

slight pickup to 0.4%. Germany’s growth in Q3 marked a slowdown from 0.4% & fell short of the forecast. Italy’s

economy (euro region's 3rd largest) grew 0.3%, resuming

expansion after stagnation in Q2. In the

Netherlands, growth was unchanged from the previous qtr at 0.7%. Previously published figures put French growth at 0.2%. In

Germany, domestic demand drove growth in Q3 as both gov & private consumption spending rose. The

global economy dragged on growth, with exports contracting slightly.

Investment in equipment also slipped while construction climbed.

Sales at US retailers rose more than forecast last month in a broad

advance after an even stronger Sep than initially estimated,

showing consumers continue to pump up the economy. A 0.8%

rise in Oct followed an upwardly revised 1% jump in the prior

month, marking the biggest back-to-back increase since March-April

2014, according to the Commerce Dept. The forecast called for a 0.6% gain. Over the last 12

months, retail sales were up the most in almost 2 years. Healthy

hiring, wage growth & limited inflation are giving Americans the

wherewithal to spend at stores, malls & online merchants. Momentum at

the start of the qtr bodes well for household purchases during the approaching

holiday-shopping season. Retail receipts

increased 4.3% from Oct 2015, the biggest advance since

Nov 2014.

Sales improved in 11 of 13 major categories for a 2nd straight month. That included the

biggest advance in 5 months at internet retailers & the strongest

month for apparel chains since Feb. Furniture outlets & restaurants were the only major categories registering a decline in Oct sales. Auto purchases remained robust, climbing 1.1% after a 1.9% increase. Retail

sales excluding automobiles & service stations increased 0.6%

after a 0.5% gain a month earlier. The figures used to calculate GDP, which exclude categories such as food services, auto

dealers, home-improvement stores & service stations, climbed 0.8%. The increase in the retail control group was the

largest since Apr & followed a 0.3% Sep gain that was

stronger than first reported.

The spectacular advance for the Dow has finally ended, but the markets remain in a state of turmoil. Treasury bonds are trying to find a floor after their decline. Junk bond funds are doing better. Oil is up on hopes for an agreement on production cuts. Money is finally buying tech stocks. These are volatile times which will not end soon.

No comments:

Post a Comment