This blog gives investors more financial information for very smart investing!

Friday, November 4, 2016

Markets crawl higher, trying to end 8 day losing streak

Dow inched up 9, advancers over decliners 3-2 & NAZ added 11. The MLP index fell 2+ to the 286s (another low shown in the chart below) & the REIT index was off a fraction in the 321s. Junk bond funds slid lower & Treasuries had a modest advance in price. Oil dropped to the 44s (more below) & gold was little changed above 1300.

US jobs continued to rise at a steady pace in Oct & wage

gains accelerated, signs that the labor market & economy made steady

progress at the start of Q4. Payrolls climbed 161K following a 191K gain in Sep (larger

than previously estimated), according to the Labor Dept. The forecast called for 173K. The jobless

rate fell to 4.9%, while wages rose from a year earlier by the

most since 2009. The figures are likely to keep the Fed on track to raise borrowing costs next month. Underlying the steady gains in employment is a balance between

hiring managers’ need to keep up with stable domestic demand and the

struggle to match more limited labor to skilled-job vacancies.

Workers have been in short supply for 13 straight

months, according to the Institute for Supply Management survey of

service-industry companies. The forecast called for a

173K advance in payrolls after a previously reported 156K

Sep increase. Revisions added a total of 44K jobs to payrolls in the previous 2 months. While

economists & policy makers largely agree that the economy is

close to full employment, blemishes remain, with the ranks of part-time

workers & long-term jobless still higher than before the last

recession. The labor force participation rate, which indicates the

share of working-age people who are employed or looking for work,

slipped to 62.8% from 62.9%, as the number of people in

the labor force declined. The underemployment rate

dropped to 9.5% from 9.7%, while the number of

people working part-time for economic reasons was little changed. 5.89M employees were

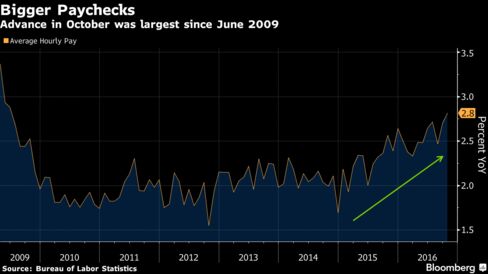

in part-time jobs but wanted full-time work. Wage gains picked up,

with average hourly earnings rising 0.4% from a month earlier to

$25.92. The year-over-year increase was 2.8%, compared with 2.7% in the year ended in Sep.

Oil headed for its biggest weekly loss in almost 10 months as hopes

faded that OPEC will be able to implement a promised deal to cut

production & ease global oversupplies. Futures dropped over 2% after falling 10% the previous 5

sessions. Prices closed yesterday at the lowest level since OPEC reached a

preliminary agreement in Algiers for the cuts, & extended losses

today after a report that Saudi Arabia threatened to raise

output if other members didn't agree to cuts. US inventories increased

by a record last week.

West Texas Intermediate for

Dec delivery dropped 82¢ (1.8%) to $43.84 a barrel after

touching $43.79, the lowest since Sep 20. Total volume was 51% above the 100-day average. Prices are down about 10% this

week, the most since the period ending Jan 15.

China stocks edged down on today but notched up its 4th straight

week of gains as signs of a stabilizing Chinese economy offset lingering

worries over the looming US election outcome. The blue-chip CSI300 index fell 0.3%, to 3354, while the Shanghai Composite Index dipped 0.1% to 3125. For the week, CSI300 rose 0.4%, while SSEC added 0.7%, both up for the 4th week in a row. Comforted by recent upbeat manufacturing & service data,

Chinese investors are turning their attention to a flurry of fresh

economic data in the coming weeks that is widely expected to reinforce

views that the economy is stabilizing. Another help at times of anxiety is the country's rigid capital

controls which may help act as a cushion against potential

overseas shocks. Most sectors dipped, dragged in particular by property &

transport stocks, as well as massive profit-taking in speculative

stocks. This dampened investors' risk appetite in a market where retail

investors remain a dominant force.

Stocks are trying to end a long losing streak. But the jobs news was no help. It was only routine, not impressive. Uneven economic fundamentals continue & the latest bets are that the Fed will hike rates next month. The bulls would like to take the Dow back over 18K, but that may have to wait as earnings from retailers will be reported.

No comments:

Post a Comment