This blog gives investors more financial information for very smart investing!

Thursday, November 3, 2016

Markets edge higher on mixed economic data

Dow rose 29, advancers over decliners 4-3 & NAZ fell 7. The MLP index dropped 2+ to the 289s (another interim low) & the REIT index was even in the 323s (still down more than 40 from this years highs). Junk bond funds were mixed & Treasuries drifted lower. Oil pulled back in the 45s & gold was also sold, taking it below 1300.

Worker productivity rose in Q3 by the most in 2

years as the economy picked up steam, offering a respite from the weak

efficiency gains that have defined the US expansion. The measure

of employee output per hour increased at a 3.1% annualized rate,

after a revised 0.2% drop in the prior qtr, according to the Labor

Dept. The forecast called for a 2.1% gain. Expenses per worker climbed at a

0.3% pace. The productivity data represent a break from the

longest consecutive string of declines since 1979, as employers

squeezed more output from existing workers. Efficiency was little

changed over the last 12 months, consistent with the long-term downtrend

as businesses have been reluctant to invest in equipment, relying

instead on more hiring. The reading for the prior qtr was initially

reported as a drop of 0.6%. Over the last 5 years, annual productivity gains averaged 0.6%, the weakest since 1978-1982.

Unit

labor costs, adjusted for efficiency gains, were forecast to

rise an annualized 1.2%. They rose 3.9% in Q2, revised from a

previously reported advance of 4.3%. Adjusted for inflation, hourly earnings rose at a 1.7% rate, after increasing at a 1.2% pace. Output climbed at a 3.4% rate, the most in 2 years, following a 1.6% gain the prior qtr. Hours worked rose at a 0.3% pace, the weakest in a year, after a 1.7% advance. Among manufacturers, productivity increased at a 1% rate in Q3 after a 0.5% decrease.

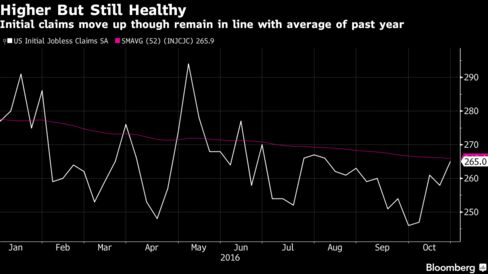

Filings for US unemployment benefits unexpectedly rose to the

highest level in almost 3 months, extending increases from a 4-decade low. Jobless claims increased 7K to 265K, according to the Labor Dept. The forecast called for a drop

to 256K. Continuing claims dropped to the lowest since 2000. Even

with the increase, initial claims are in line with the 264K average

for 2016, as a dwindling pool of skilled & experienced job hunters

keeps employers from laying off workers. While payroll gains have cooled

from last year’s pace, they probably remained solid in Oct, with a

175K rise projected the gov report

due tomorrow.

Filings

for unemployment benefits have been below 300K for 87 straight weeks, the longest streak since 1970 & a level typical for a healthy

labor market. Claims touched 246K in the week ended Oct 1, the lowest since 1973. The 4-week average of claims, a less-volatile measure than the weekly

figure, increased to 257K from 253K in the prior week. The

number continuing to receive jobless benefits dropped 14K to 2.03M & the unemployment rate

among people eligible for benefits held at 1.5%.

A gauge of US service-sector activity fell in Oct, a sign of decelerating growth in key sectors of the economy. The Institute for Supply Management said its

nonmanufacturing index fell to 54.8 from 57.1 in Sep. A

reading above 50 signals expansion while a reading below 50 indicates

contraction. The index has run above the 50 threshold for 81 straight months. The forecast called for a

reading of 56.0. Drops in business activity, new orders & employment

pulled the overall reading down. Americans' spending on services accounts for around 2/3

of overall personal-consumption expenditures & the service sector

provides the bulk of jobs. Job growth was largely concentrated in service

industries such as professional & business services, health care,

retail & restaurants & bars. A separate measure of service-sector activity from private data

provider Markit showed its services business activity index rose to 54.8

in Oct from 52.3 in Sep.

Stocks are looking for direction. Chances are the jobs report tomorrow will give few new insights into where the economy is going. Election jitters are another dark cloud hanging over the market & that will be around until Wed. Next week should see earnings reports from retailers which will also give their outlook for the important holiday season. Times are tough for stocks.

No comments:

Post a Comment