This blog gives investors more financial information for very smart investing!

Monday, February 1, 2016

Markets begin new month lower on weak economic data

Dow dropped 112, decliners over advancers 5-2 & NAZ pulled back 32. The MLP index sank 8+ to the 246s & the REIT index lost 1+ to the 311s. Junk bond funds edged lower & Treasuries were sold. Oil slipped back to the 32s & gold is strong while stocks are weak.

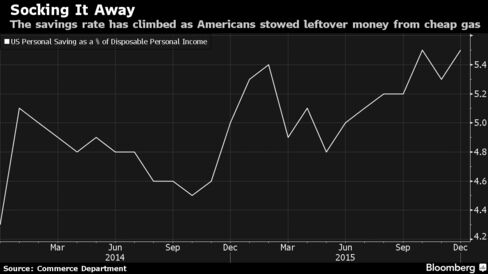

Household spending cooled in Dec as Americans used gains in incomes to boost their savings. Consumer

purchases were little changed after a 0.5% advance in Nov

that was bigger than previously estimated, according to the Commerce Dept. The forecast called for a 0.1% increase. Incomes climbed 0.3% for a 2nd month. Household

purchases moderated in Q4, contributing to a slowdown

in the economy as businesses slashed investment & worked to pare down

inventories. A spending rebound, powered by sustained job gains & low

inflation, will be needed to reinvigorate growth. The previous month's reading

was initially reported as a 0.3% increase. Incomes were projected

to rise 0.2%. Disposable income, or money left over after

taxes, increased 0.4% in Dec from the prior month after

adjusting for inflation & grew 3.5% in 2015, the most in 9

years. The saving rate climbed to 5.5% from 5.3% & matched the highest since the end of 2012.

The price index tied to consumer spending decreased 0.1% & from a year earlier, the gauge was up 0.6%.

This inflation measure is preferred by Federal Reserve policy makers &

hasn't met their target since Apr 2012. Stripping out the volatile

food & energy components, the price measure was unchanged from the

month before & up 1.4% in the 12 months ended Dec. After

adjusting for inflation, which generates the figures used to calculate GDP, purchases climbed 0.1% after a

0.4% gain in Nov.

China's official factory gauge signaled a record 6th straight month of

deterioration, raising the stakes for policy makers struggling to prop

up the economy amid a 2nd bear market in stocks since Jun & a

currency at a 5-year low. The purchasing managers index dropped to a 3-year low of 49.4 in

Jan, the National Bureau of Statistics said. That compared

with an estimate of 49.6.

Numbers below 50 indicate conditions worsened. The official services

index also fell, while a private PMI survey signaled the industry shrank

an 11th month. The reports

could complicate the dilemma for policy makers: add monetary stimulus to

help stem the slowdown in growth, or avoid more easing that could

exacerbate record capital outflows & put more pressure on the yuan.

Chinese stocks fell, extending Jan's steepest monthly rout since

2008, threatening to further shake investor faith in how top officials

can manage the economy. The

People's Bank of China cut the main interest rate 6 times from late

2014 to late 2015 to a record-low 4.35%. It also has made a

series of reductions to the reserve-requirement ratio for big banks,

allowing them to keep less cash locked up at the PBOC. Meanwhile the

US Federal Reserve in Dec raised rates for the first time in almost a

decade. China’s capital outflows jumped in Dec, with the

estimated 2015 total reaching $1T, amid a 6.9% economic expansion last year that was the

slowest in a qtr century. The

Shanghai Composite Index was down 1.8%, bringing

the YTD drop to 24%. The official manufacturing

gauge's 6 months below 50 is the longest stretch of readings below

that level in NBS data since the start of 2005. The PMI slumped last

month because of weak demand & efforts to reduce overcapacity. Indicators for new export orders & imports

also decreased from a month earlier. The non-manufacturing PMI for services edged down to 53.5 last month from a 16-month high of 54.4 in Dec. A

private manufacturing survey showed some improvement,

though it’s been below 50 since Feb. The Caixin China Manufacturing

PMI rose to 48.4 last month from 48.2 in December & new orders rose from

the prior month, climbing to the highest level since Jun.

US manufacturing shrank in Jan for a 4th consecutive

month as businesses cut staffing plans. Growth resumed in new orders & production, indicating some stabilization in the industry. The 48.2 reading for the Institute for Supply Management index

followed Dec's 48 level that was the weakest since Jun 2009. The results were

lower than the 48.4. Levels less than 50 for the gauge indicate contraction. Factories are buffeted by persistent weakness in the oil industry,

the stronger dollar & cooling overseas markets that also limited

growth last qtr. The report showed the gauge of new orders, a

leading signal for production, grew for the first time in 3 months,

which would help manufacturing eventually strengthen. The new orders gauge rose to 51.5, the strongest since Aug, from

48.8 & a measure of production climbed to 50.2, the first expansion in 3 months, from 49.9. The factory employment index dropped to 45.9, the weakest since Jun 2009, from the prior month's 48. The measure of export orders dropped to a 4-month low of 47 last month from 51. The gauge of factory inventories held at 43.5, while customer

stockpiles stayed at 51.5. The index for supplier deliveries was little

changed at 50 after 49.8. The index of prices paid were the same as the

previous month’s reading of 33.5 (the lowest since Apr 2009).

The prices measure has been contracting since Nov 2014. Manufacturing struggles at the start of 2016 are an extension of

late-2015 weakness, when sluggish capital spending, bloated stockpiles & a decline in exports damped US growth.

The early signals are this will be another dreary month for the stock market. The 2 biggest economies in the world started Feb with feeble economic data. Oil is heading south again as the excitement over possible production cuts is fading fast. Dow is back down to minus 1K+ YTD.

No comments:

Post a Comment