This blog gives investors more financial information for very smart investing!

Thursday, February 25, 2016

Markets crawl higher on factory orders data

Dow climbed 24, advancers of decliners 5-4 & NAZ gained 22. The MLP index fell 3+ to the 342s & the REIT index rose 2+ to the 309s. Junk bond funds drifted lower & Treasuries advanced. Oil slid back to the 31s & gold was a tad lower.

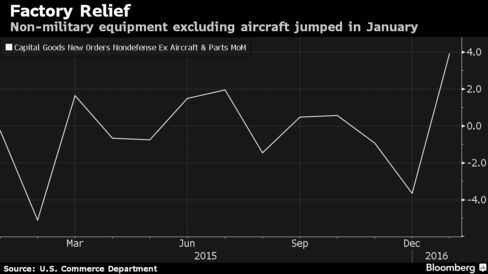

Orders for US capital goods rebounded in Jan by the most since

Jun 2014, representing a pause in the manufacturing downturn. Bookings

for non-military equipment excluding commercial aircraft jumped 3.9%, more than forecast, after a 3.7% decrease in Dec

that was smaller than previously reported, according to the Commerce

Dept. Orders for all durable goods rose 4.9%, the most since Mar.

The

increase was broad-based, from cars & computers to machines &

metals, & a sign that domestic demand is a source of support for

manufacturers battered by lukewarm overseas markets. At the same time,

the outlook for capital spending among miners, farmers & well drillers

has dimmed because of plunging commodity prices. Shipments of non-defense capital goods

excluding aircraft, used in calculating GDP, decreased 0.4% last month. They were revised up to a 0.9% increase in Dec, the largest advance since Jun, from a

previously reported 0.2% gain. The

forecast projected total

orders would increase 2.9%. A 54.2% surge in bookings for

commercial aircraft helped propel the gain & that

followed a 29.1% slump the prior month even though industry data

showed a jump in bookings for planes. Excluding

transportation equipment demand, which is volatile from month to month,

bookings increased 1.8% after a 0.7% decline

the prior month. Demand for

non-defense goods rose 4.5% after falling 2.5%. Bookings

for machinery climbed 6.9%, the most in 3 years.

Orders for motor vehicles & parts were up 3%, the biggest gain

in 6 months, while demand for communications equipment registered the

strongest advance since Nov 2014. The increase in orders came

as sales also rose, helping factories pare stockpiles.

The number of Americans filing applications for unemployment benefits

rose last week from a 3-month low, in part reflecting the typical

swings during holiday periods. Jobless claims increased 10K

to 272K, according to the Labor Dept. The forecast called for 270K. The average over the past 4

weeks was the lowest this year.

The 4-week moving average decreased to 272K, the lowest since

mid-Dec, from 273K. The number continuing to

receive jobless benefits fell 19K to 2.25M. The unemployment rate among people eligible for benefits

held at 1.7%. Since

early Mar, claims have been below the 300K level that is typically consistent with an improving job market.

China's stocks tumbled the most in a month as surging money-market

rates signaled tighter liquidity & the offshore yuan declined for a 5th day. The Shanghai Composite Index sank 6.4%, with about 70 stocks falling for each that rose. Industrial &

technology companies led losses. The overnight money rate, a gauge of

liquidity in the financial system, climbed the most since Feb 6. The

plunge in equities underscores the challenge for China’s policy makers

as they seek to project an image of stability in the financial

markets as the economy slows.

Besides

signs of tightening liquidity, stocks tumbled amid

concern recent gains weren't justified by fundamentals & policymakers

may introduce policies to restrain housing-price gains in some of the largest cities. The overnight

repurchase rate increased 14 basis points to 2.11%. The

first indicators for China's economy this month signal its slowdown

hasn't bottomed out yet, despite banks extending record new loans in

Jan. Private gauges of manufacturing & services fell to new lows, a

reading of business confidence slipped, & interest in small &

medium sized businesses deteriorated. If confirmed in

official data for Feb that starts to roll out from Mar 1, such

weakness would suggest a slowdown in the old growth drivers may

be deepening. Today’s declines almost

erased a 10% rebound in the benchmark equity index from a Jan

low. The Shanghai Composite has fallen 23% this year, the

world's worst performer after Greece.

The bulls retained some influence after yesterday's recovery in the PM. The favorable report on orders for capital goods in the US was helpful. But the energy segment, a large part of the economy, is hurting badly & the goings on in China continue to be unclear with a strong bias on the negative side. Dow is maintaining its modest rise in Feb, although down almost 1K YTD.

No comments:

Post a Comment