This blog gives investors more financial information for very smart investing!

Tuesday, March 1, 2016

Markets advance on auto sales data

Dow surged 179, advancers over decliners 3-1 & NAZ jumped up 69. The MLP index slid back fractionally to the 249s & the REIT index shot up 5 to the 315s. Junk bond funds climbed little higher & Treasuries were sold while stocks rallied. Oil was flattish after recent strength & gold declined.

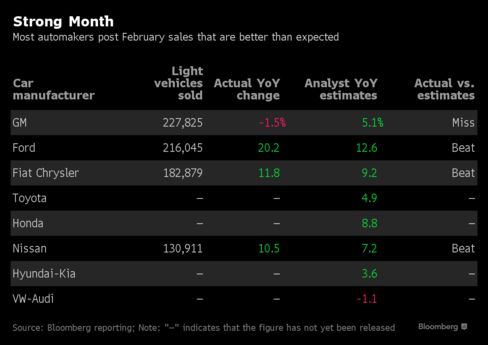

Ford (F) light vehicle sales soared 20% in Feb,

while Fiat Chrysler (FCAU) deliveries climbed 12%. Both

far exceeded estimates thanks to promotions tied to the Presidents Day holiday & continued strong demand for sport utility vehicles & pickups.

Nissan also beat estimates, but General Motors (GM) missed. Ford,

projected to report a 13%, topped that in

all 3 categories: cars, SUVs & pickups. FCAU, projected

to report a 9.2% increase, extended its US sales-gain streak to

71 months. Jeep deliveries advanced 23% from a year earlier to

68K, led by the Cherokee & Grand Cherokee. The SUV brand reported

its best Feb ever, as did Ram pickups, sales chief

Reid Bigland said.

Automakers & dealerships layered on discounts during the long holiday weekend to

catch buyers who might have put off purchases when a Jan storm

dumped 2 feet of snow in eastern US. Nissan

also beat estimates with an 11%. However GM sales fell 1.5% to 227K vehicles, missing the

estimate for a 5.2% gain. GM cut back sales of

low-priced cars to rental agencies by 16K vehicles (39%),

while retail sales rose 7%. If GM had matched rental fleet sales

from this time last year, its total sales would have been up 7%,

said Kurt McNeil, VP of US sales. “We’re still

very bullish on the market,” he added. “Jobs data is

strong, fuel prices are at historic lows and interest rates are low. We

think it could potentially be a record year.” Ford's surge was

especially strong among sport utility vehicles The

estimate for last month's annualized selling rate, adjusted for

seasonal trends, was 17.6M vehicles, an increase

of 1.2M from the pace a year earlier & would mark the best

Feb since 2000. FCAU projected a 17.9M rate,

including medium & heavy-duty trucks, which typically account for at

least 200K. GM said the light-vehicle rate was probably 17.7M.

Factory activity in Feb shrank less than forecast as gains in

new orders & production provided signs that the beleaguered industry

could soon stabilize. The Institute for Supply Management index

climbed to 49.5, the highest since Sep, from 48.2 in Jan. While the

reading was just shy of 50, the dividing line between contraction &

expansion, last month's improvement corroborates other industry reports

that suggest the manufacturing slump may be easing. Factories have

been plagued by a steady stream of headwinds since mid-2014, including

soft overseas markets, a strengthening dollar, weakness in the

capital-intensive oil industry & a buildup in inventories that reduced

the need for additional production. As those hurdles start to fade,

factories should also find a source of strength in domestic demand,

which is being boosted by consumers with solid job gains & a nascent

pickup in wage growth.

The forecast called for 48.5. The

new orders gauge was 51.5, matching the Jan reading (the highest since Aug). The production measure climbed to 52.8, a 6-month high, from 50.2. The employment index increased to 48.5

from 45.9, indicating factories trimmed staff at a slower pace. Shipments abroad continued to be pressured as the stronger $ & soft global demand combine to make it harder for foreign

markets to purchase US goods. Export orders measure decreased to

46.5, the lowest in 5 months, from 47 in Jan. Exports have

contracted in eight of the past 9 months. The gauge of factory

inventories improved to 45, meaning stocks were being cut at

a slower pace, from 43.5, while customer stockpiles declined to 47 from

51.5. This was the first reading lower than 50, meaning factory

managers no longer believe their customers have too many goods on hand,

since Jul. The report also showed that while prices continue to

fall, the pace of decline is starting to moderate. The prices-paid index

improved to 38.5 from 33.5. The measure has been contracting since

Nov 2014. The ISM report adds to evidence that the pressure

on manufacturing may be easing somewhat.

Federal Reserve Bank of NY pres William C. Dudley said

that while he still expects inflation to reach the central bank's 2% target over time, he's lost some confidence in that prediction

following recent turbulence in financial markets. “On balance, I am somewhat less confident than I was before,” Dudley said. “Partly,

this reflects my assessment that uncertainty to the outlook has

increased and that downside risks have crept up.”

The

vice chair of the policy-setting FOMC was

speaking at a rare joint conference with the People's Bank of China. At

the same venue, PBOC Deputy Governor Chen Yulu warned that a

strengthening $ could fuel a crisis in emerging markets, & said

the central banks of the world's top 2 economies should work more

closely to counter a trend of weakening global economic-policy

coordination. Dudley said that “tighter

financial conditions abroad do spill back into the U.S. economy, and

policy makers must take this into account in their assessment of

appropriate monetary policy." At the same time, market volatility won't

dictate policy decisions. He has so far marked down his forecast for US

economic growth this year “very modestly,” & still believes it will

average around 2%, enough to continue reducing labor-market slack & stoke inflation. Although

Dudley said his “overall outlook has not changed substantially,”

downside risks have increased, & could trigger revisions to the

outlook if they continue. He flagged declines in market-based measures

of inflation expectations as well as those derived from consumer surveys

as “concerning,” & added that internal Fed models assigned greater

odds to the economy disappointing policy makers' projections than

exceeding them. “At this moment, I judge

that the balance of risks to my growth and inflation outlooks may be

starting to tilt slightly to the downside,” Dudley said. “The recent

tightening of financial market conditions could have a greater negative

impact on the U.S. economy should this tightening prove persistent.”

The first economic reports were favorable. Auto sales are doing well, but it's difficult to see them rising far above present levels which are already near record levels. Oil trading is quit today, but that will continue to cause major swings in the stock market & high volatility will continue for some time. Dow is still down more than 700 YTD.

No comments:

Post a Comment