This blog gives investors more financial information for very smart investing!

Thursday, March 10, 2016

Markets waver after ECB provides more stimulus

Dow slid back 4, decliners just ahead of advancers & NAZ inched up a fraction. The MLP index lost 1+ to the 257s & the REIT index added 1+ to the 323s. Junk bond funds rose & Treasuries were sold. There was profit taking in oil while gold was bid higher.

Mario Draghi delivered interest-rate cuts, more bond purchases & a

potential subsidy to lenders in a renewed attack against the threat of

deflation & said the ECB is done with lowering borrowing costs for now. The

ECB reduced the rate

on cash parked overnight by banks by 10 basis points to minus 0.4% & lowered its benchmark rate to "0." Bond purchases were

increased to €80B ($87B) a month from €60B, & corp bonds will now be eligible. A new series of

long-term loans to banks will begin in Jun “The

Governing Council expects key interest rates to remain at present or

lower levels for long period of time and well past the horizon of our

net asset purchases,” Draghi said. Based on the current view, “we don’t

anticipate it will be necessary to reduce rates further.” He ECB said that:

Interest rates will remain at present or lower levels for an extended period of time

The outlook for growth has been revised down, reflecting weakening global prospects

2016 GDP revised down to 1.4% from 1.7%

2017 GDP revised down to 1.7% from 1.9%, GDP to be 1.8% in 2018

Inflation forecast for 2016 slashed to 0.1% from 1%

Inflation to be 1.3% in 2017, will average 1.6% in 2018

The new round of

targeted refinancing operations will start in Jun. The central bank

said the interest rate “can be as low as the interest rate on the

deposit facility,” indicating that it may pay lenders to

borrow from it.

Filings for US unemployment benefits fell last week to the lowest

level in 5 months as the number of dismisals remained consistent with a

solid labor market. Jobless claims dropped 18K to 259K, the fewest since mid-Oct, from a revised

277K in the prior week, the Labor Dept said. The forecast called for 275K. Employers are demonstrating an appetite to add to staff & hold off

on layoffs based on a brighter US outlook, even as overseas growth

sputters & financial markets remain volatile. A tighter job market is

slated to slow the pace of hiring this year as workers await a bigger

pickup in wages. Last

week's reading approached the 4-decade low of 255K reached in

mid-Jul, marking a full year of weekly filings lower than the 300K

level that economists say is consistent with strength in the labor

market. The 4-week average of claims declined to 267K from 270K in the prior week. The

number continuing to receive jobless benefits dropped 32K to 2.23M & the unemployment rate

among people eligible for benefits fell to 1.6% from 1.7%.

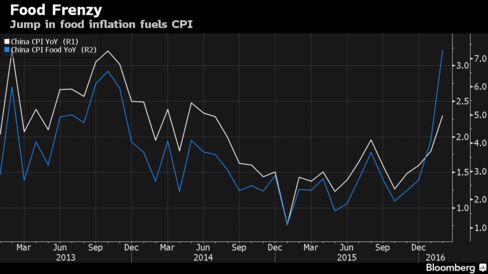

China's consumer price rose the most since mid-2014 in Feb as

food costs jumped amid the week-long Lunar New Year holidays, where

millions consume on roast pork, duck, seafood & vegetables. The

consumer-price index rose 2.3% from a year earlier,

up from 1.8% in Jan, as food prices surged 7.3%.

Raising question marks over the durability of that pickup, non-food

prices moderated from a month earlier to a 1% increase &

services inflation slowed.

The

producer-price index fell 4.9%, narrowing from a 5.3%

decrease in Jan, extending declines to a record 48 months. Stabilization

in prices, if sustained in coming months, will ease concerns over deflation, which discourages new investment & erodes

profit margins. Still, CPI remains well below the gov target

for 3% this year, meaning there’s no constraint yet for easier monetary settings.

More money has done much for the Euro economy, so the solution from the ECB is to throw even more money out there. Markets drifted lower. Maybe they're tired of the same old gimmicks that don't get results. Dow is flirting with 17K, can't make up its mind whether to go above or below. Following a stellar rise in the prior month, it has been trading sideways for a week.

No comments:

Post a Comment