This blog gives investors more financial information for very smart investing!

Wednesday, March 16, 2016

Markets waver on mixed economic data

Dow was off 4, advancers over decliners 3-2 & NAZ added 10. The MLP index rose 3+ to the 262s & the REIT index slid back 1+ top the 326s. Junk bond funds were a little higher & Treasuries declined. Oil bounced back after selling in the last 2 days & gold was flattish.

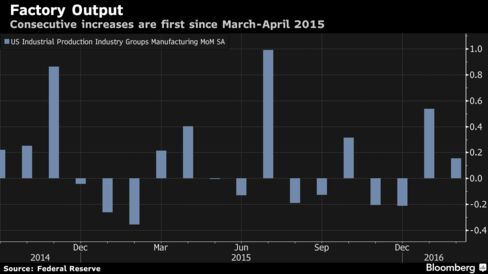

Factory production rose in Feb for a 2nd month, boosted by

demand for business equipment & indicating manufacturing may be

starting to stabilize. The 0.2% increase in output followed

a 0.5% gain in Jan, according to the Federal Reserve. It marked the first back-to-back advance since Mar-Apr

2015. Total industrial production dropped 0.5% as utility output

plunged by the most since Mar 2007.

American

factories might be catching a break from a modest climb in energy

prices even as they battle $ appreciation in a bid to regain

momentum after months of malaise. Manufacturing is struggling to

reaccelerate amid tepid global growth that’s holding back the US

economy. Manufacturing

output, which accounts for about 12% of the economy, was

projected to rise 0.1% last month & total industrial production was forecast to decline 0.3%. Capacity utilization, which measures the amount of a

plant that is in use, fell to 76.7% in Feb from 77.1%

the prior month. Manufacturing capacity was unchanged at 76.1%. Warmer-than-usual

temperatures in Feb depressed utility output by 4% after a

4.2% advance in Jan. Mining,

including oil drilling, dropped 1.4% after a 0.7% decline. Well drilling plunged 15.6% last month.

US consumer prices, excluding food & fuel, climbed more than

forecast in Feb for a 2nd month, adding to signs inflation is

moving closer to the Fed target. The overall cost of

living fell amid cheaper fuel. The core measure, which

strips out volatile food & fuel, rose 0.3% from a month

earlier, the same as in Jan, figures according to the Labor Dept. The last time there were back-to-back

gains of 0.3% was in early 2001. The overall consumer-price index

declined 0.2%, matching the forecast.

Price

pressures are starting to stir more broadly after plunging fuel costs & the stronger $ kept inflation subdued through 2015. The consumer price gauge increased 1% in the 12

months ended Feb, after a 1.4% year-over-year advance the

prior month. The core CPI

measure, which excludes volatile food & fuel costs, rose 2.3%

from Feb 2015, the most since May 2012, after rising 2.2% in

the prior 12-month period. The projection called for the core gauge to rise 0.2% from the previous month. Energy costs decreased 6% from a month earlier & food prices rose 0.2%. The 1.6

percent jump in apparel prices last month was the biggest in 7

years. Higher prices for shelter, including rents & hotel rates,

have been helping to put a floor under inflation even as cheaper energy

bills & the strong $ exert downward pressure. The Fed's

preferred gauge of inflation, which is the

personal consumption expenditures measure, hasn’t matched the Fed 2% goal since Apr 2012.

New-home construction in the US rose more than forecast

in Feb, led by the strongest single-family building in more than 8 years, signaling continued confidence in demand for residential

real-estate. Housing starts in Feb climbed 5.2% to a 1.18M

annualized rate from a 1.12M pace the prior month, the Commerce

Dept said. The forecast was 1.15M. Permits, a proxy

for future construction, fell, suggesting any additional gains in coming

months will be limited. Steady employment growth & a low level of layoffs are creating the

kind of job security needed to help households feel comfortable buying a

home. An improvement in the selection of available properties, in

addition to a pickup in wage growth, will be important in helping lure

more first-time buyers & shift the housing recovery into a higher

gear. Building permits dropped 3.1% in

Feb to a 1.17M annualized rate after a 1.2M pace the

month before. They were projected to be little changed at 1.2M. Construction of single-family houses increased to an 822K rate, the most since Nov 2007. Work on multifamily homes, such as apartment buildings, rose to a

356K rate. 3 of 4 regions had an increase in starts, paced by

a 26.1% advance in the West & construction sank 51% in the Northeast. On a year-to-year basis, total housing starts were up 31% in Feb. Mild winter weather is typically a positive for the housing industry

as more construction can take place. The pace of any rate increases will likely be of high importance for

the housing industry, as cheap borrowing costs have offered support to

buyers throughout the recovery.

No comments:

Post a Comment