This blog gives investors more financial information for very smart investing!

Friday, March 4, 2016

Markets edge higher after a mixed February jobs report

Dow went up 45 after starting the day lower, advancers over decliners 2-1 & NAZ gained 5. The MLP index climbed 1 to the 266s, extending its recent rally, & the REIT index lost 1 to the 321s. Junk bond funds fluctuated & Treasuries retreated. Oil inched higher, closing in on the important 35 resistance level, & gold was higher (see below).

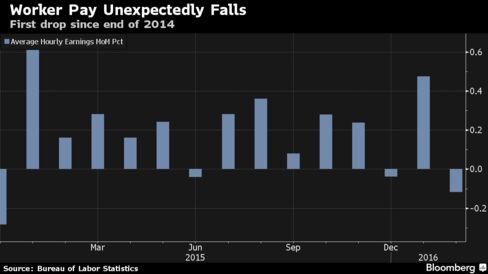

Employers added more workers in Feb than projected but wages

unexpectedly declined, dashing hopes that reduced slack in the labor

market was starting to benefit all Americans. The 242K gain

followed a 172K rise in Jan that was larger than previously

estimated, according to the Labor Dept. The jobless rate

held at 4.9% as people entered the labor force & found work.

Average hourly earnings dropped, the first monthly decline in more than a

year, & workers put in fewer hours. A job market in good health

will reinforce job security & encourage Americans to spend, buffering

the US from the ill-effects of global economic weakness. At the same

time, stronger wage growth would help move inflation closer to the Federal

Reserve's goal. The forecast

called for a 195K advance & Jan was initially reported as a 151K

increase. The unemployment rate showed

that the labor force expanded by more than a ½M &

almost all found work. Joblessness was projected to hold at 4.9%, an 78-year low. Average

hourly earnings dropped 0.1% from the prior month, the first

decline since Dec 2014.

Worker pay increased 2.2% over the 12 months ended in Feb,

less than the 2.5% forecast. Wage growth

has been hovering just above 2% year-over-year on average since

the current expansion began in mid-2009.

The average work week for all workers declined 12 minutes to 34.4 hours. Retailers

posted strong employment gains for a 2nd month, along with the

health care industry. Payrolls at retailers climbed about 55K in

Feb after a 62K advance a month earlier, while health care

employment increased 57K. Payrolls at factories declined 16K after a 23K gain & construction companies added 19K workers. The

participation rate, which shows the share of working-age people in the

labor force, jumped to 62.9%, the highest since Jan 2015.

Gold cruised to a bull market, heedless of rebounding stock markets,

as traders expect central banks to curb yields on other investments in

an effort to spur economic growth. The metal is up more than 20% since a Dec low,

outpacing all major assets. Gold rose as investors

weighed a surge in US payrolls against an unexpected decline in wages.

Looser

policy & the lower rates on securities that tend to follow add to the

appeal of gold, which yields nothing. The metal is also a haven in

times of crisis & slow growth. Bullish sentiment in gold

is reflected in exchange-traded funds (ETFs). Investors raised holdings in

gold-backed ETFs by 259 metric tons so far this qtr, which would be

the biggest quarterly gain since Jun 2010. Holdings are rising after 3 straight years of withdrawals.

The US trade deficit widened more than expected in Jan as a

strong $ & weak global demand helped to push exports to a more

than 5½ year low, suggesting trade will continue to weigh

on economic growth in Q1. The Commerce Dept said the trade gap increased

2.2% to $45.7B & the Dec trade deficit was revised up to

$44.7B from the previously reported $43.4B. Exports have

declined for 4 straight months. The forecast was for a widening of the trade deficit to $44.0B. When adjusted for inflation, the

deficit increased to $61.97B from $60.09B in Dec. Trade subtracted a quarter of a percentage point from GDP in Q4, helping to hold down growth to a

tepid 1.0% annual rate. Exports of goods fell 3.3% to $116.9B,

the lowest level since Nov 2010. Overall exports of goods &

services dropped 2.1% to their lowest level since Jun 2011. There were declines in food exports, which were the weakest since

Sep 2010. Industrial supplies & materials exports fell to their

lowest level since Mar 2010. Petroleum exports also fell, touching

their lowest level since Sep 2010. Exports of non-petroleum products were the weakest in 5 years. Imports fell 1.6% to $180.6B, the lowest

level since Feb 2011. Import growth is being constrained by ongoing

efforts by businesses to reduce a stockpile of unsold merchandise. Lower oil prices as well as increased domestic energy production

are also helping to curb the import bill. Automobile imports were, however, the highest on record. The US-China trade deficit rose 3.7% to $28.9B.

Stocks continue to digest the news while waiting on developments. The jobs created in Feb sounds good, but wages data was not. Earnings continue to come in mixed while Q1 estimates are being reduced. The oil powers are still meeting, trying to come up with solutions to the oil global glut. And the Chinese economy is stuck in neutral. But Dow has had a very good month & the FOMC meeting is less than 2 weeks away.

No comments:

Post a Comment