Dow rose 25. advancers over decliners 5-4 & NAZ gained 30. The MLP index lost a fraction to the 301s following recent strength & the REIT index sank 8+ to the 337s. Junk bond funds edged higher & Treasuries sold off, taking the yield on the 10 year Treasury over 1.8%. Oil crawled higher after weakness at the opening & gold drifted lower.

Oil edged lower, off 2016 highs, as the impact of unplanned supply disruptions from

Nigeria & Canada were tempered by rising supplies from elsewhere. Unscheduled supply outages in Nigeria & Canada amounting to

around 2M barrels per day (bpd) have supported oil prices in

recent weeks. But analysts warned that rising supplies from other countries could weigh on prices once supply disruptions ease. Data from Iran shows oil exports from the country are recovering faster than expected. Exports from the OPEC member country are set to surge in May to

2.1M bpd, nearly 60% above their level a year ago, with

European shipments recovering to about ½ of their pre-sanction

levels, according to a source with knowledge of the country's crude

lifting plans. Saudi Arabia's crude oil exports in Mar, however, fell slightly

to 7.541M bpd from 7.553M in Feb.

China's benchmark stock index closed at the lowest level in 2½

months, after comments from Federal Reserve officials

rekindled prospects of a US interest rate rise as early as Jun. The Shanghai Composite Index lost 1.3% to 2807, the lowest since Mar 1. The blue-chip CSI300 index

fell 0.6%, to 3068. Sentiment in China had already been weak in recent months amid

concerns that signs of recovery in its economy may be short-lived &

worries that policymakers are growing more cautious about providing

additional stimulus as bad debts mount. Confidence was further hit by overnight weakness in

NY, after strong US consumer prices & other economic

data added to the case for a rate increase sooner.

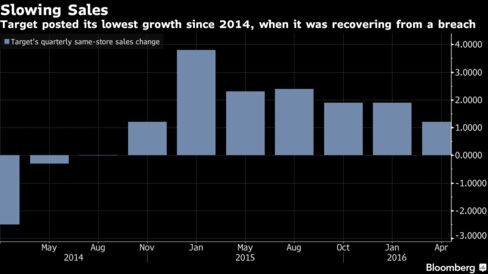

Target, A Dividend Aristocrat, fell the most in 7 years after

quarterly sales missed estimates & the chain

delivered a disappointing forecast, adding to evidence that the biggest

retailers are suffering from a slump. Same-store

sales gained 1.2% in Q1. Analysts had

predicted 1.6%. CEO Brian Cornell cited “an increasingly volatile

consumer environment” & colder weather in the Northeast, adding his

voice to the chorus of retailers complaining of sluggish demand. As it

copes with the slowdown, the company expects same-store sales to range

from flat to down as much as 2% in Q2. But

Cornell said it is too early to tell whether the pullback by consumers

will persist through the rest of the year. “We

have seen the impact of climate and a more cautious consumer,” Cornell

added. “We haven’t seen anything from a

structural standpoint that gives us pause.”

Cornell said e-commerce sales were a

“bright spot.” They grew 23%, though that was a

slowdown from the 38% growth last. TGT

also hasn’t seen a material impact from a boycott effort over

bathrooms, he said. Conservative groups targeted the chain after its

announcement last month that it would allow transgender customers to use

the restroom of their choice. The move has drawn protests, but it’s

only affected a “handful of stores,” Cornell said. Meanwhile,

the company has successfully used cost cuts to bolster profit. It

reported EPS of $1.29, beating the estimate of $1.19. “We plan to successfully implement our

long-term strategy, even in the face of a challenging short-term

consumer landscape,” Cornell added. The stock tumbled 6.80 (9%). If you would like to learn more about TGT, click on this link: club.ino.com/trend/analysis/stock/TGT?a_aid=CD3289&a_bid=6ae5b6f7

Retail earnings tell the story that the recovery is not doing as well as it should. Oil is back to 2016 highs & fears about raising interest rates faded. But Dow remains overbought, vulnerable to disappointing news.

No comments:

Post a Comment