This blog gives investors more financial information for very smart investing!

Friday, May 6, 2016

Markets fall after disappointing April jobs report

Dow dropped 77, decliners over advancers 4-3 & NAZ fell 31. The MLP index lost a fraction to the 293s & the REIT index was off 1+ to the 342s. Junk bond funds edged higher & Treasuries slid lower. Oil recovered some of its weekly loss & gold was also higher.

Employers in Apr added the fewest number of workers in 7 months & the jobless rate held steady as subdued economic growth

prompted a more moderate rate of hiring. The 160Kgain in

payrolls followed a revised 208K rise in Mar, according to the Labor Dept. The forecast called

for a 200K Apr advance. The jobless rate, projected to ease, stayed

at 5%, while wage growth accelerated. Industries that

showed strong Q1 job growth pulled back, with retailers

cutting payrolls by the most in 2 years & construction companies

adding the fewest positions since Jun. More tempered additions to

headcounts shows hiring managers are adjusting in the wake of economic

growth that has slowed for 3 straight qtrs. Mar was initially

reported as a 215K increase & revisions to prior reports subtracted a

total of 19K jobs to payrolls in the previous 2 months. The bright spot in the

report was in worker wages. Average hourly earnings climbed 0.3% from the prior month after a 0.2% advance. Worker pay

increased 2.5% over the 12 months ended in Apr after a 2.3% gain a month earlier. Wages been hovering just above a 2% yearly gain on average since the current expansion began in mid-2009. The average work week for all private workers rose by 6 minutes to 34.5 hours. Retailers

reduced payrolls by 3.1K, the most since Feb 2014.

Economists had projected retail hiring would ease up after a

Q1 surge of 157K. The underemployment rate, which

includes part-time workers who'd prefer a full-time position & people

who want to work but have given up looking, fell to 9.7% from

9.8%.

Oil headed for its first weekly decline in more than a month as

rising US stockpiles & OPEC production cushioned the impact of

declines in North American output. US

inventories rose to the highest since 1929 while production slid the

most in 8 months last week.

Canada's supplies are sufficient to cover production losses from fires

in the oil-sands region. OPEC output climbed in

Apr, including gains from Iran & Iraq.

Oil

has rebounded after slumping to the lowest since 2003 earlier this year

amid signs the global glut will ease as US output declines. The

nation's stockpiles swelled to 543M barrels last week,

according to the Energy Information Administration. Inventories are expected to rise further to a record before starting a seasonal slide.

The debt of states last year remained below its all-time high

from 2013, showing officials were hesitant to borrow even with interest

rates near record lows & the recession 6 years in the past. Their

net tax-supported debt edged up 0.6% in 2015 to $512,

according to a Moody's Investors Service. In

2014, the figure fell for the first time in almost 3 decades, from

the record high of $516B. After contending with a long

recovery from the recession, states & cities have used the $3.7T municipal-bond market in recent years largely for refinancing

instead of running up new debt for public works. There hasn't been a

more attractive time in decades for lawmakers to issue long-term bonds:

the yield on a Bond Buyer index of 20-year municipal general-obligation

bonds fell in Feb to the lowest since 1965.

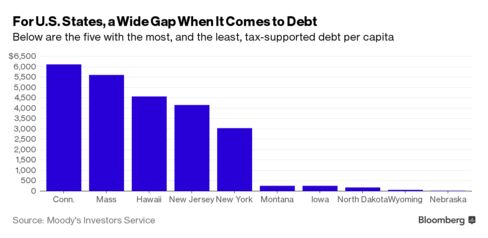

Connecticut

retained its spot at the top with $6155 of

net tax-supported debt per resident, up from $5491 last

year. Massachusetts, Hawaii, NJ & NY

round out the top 5, each with more than $3K

per person. Nebraska, Wyoming, North Dakota, Iowa & Montana have the

smallest burdens, at less than $250 per resident.

The jobs report did not bring out buyers & the market is selling off as I write. Dow is barley up YTD & down about 500 from its recent high. May is not shaping up as a good month for the overbought stock market.

No comments:

Post a Comment