This blog gives investors more financial information for very smart investing!

Wednesday, May 4, 2016

Markets drift lower on mixed economic data

Dow gave up 31, advancers barely ahead of decliners & NAZ fell 15. The MLP index lost 4+ to the 289s & the REIT index added 1 to the 339s. Junk bond funds pulled back & Treasuries were sold. Oil advanced & gold declined.

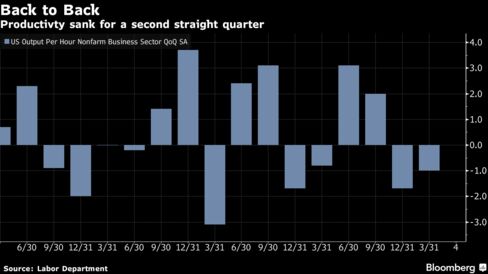

US worker productivity decreased for a 2nd straight qtr &

employer costs for labor climbed by the most in more than a year. The

measure of employee output per hour fell at a 1% annualized rate

from Jan thru Mar after a 1.7% decline in Q4. The estimate was for a 1.3% retreat. Labor costs jumped 4.1%, more than forecast.

Employers

have steadily beefed up headcounts to meet demand even as growth

softened the past 2 qtrs. At the same time, they’ve been hesitant

to ramp up investments in efficiency-boosting equipment, meaning

productivity will likely continue to languish. The productivity data showed

expenses per worker picked up in Q1 from a 2.7%

rate in Q4. These unit labor

costs, which are adjusted for efficiency gains, were forecast to climb

3.3%. Adjusted

for inflation, hourly earnings increased at a 3.4% rate in Q1, the most in a year, after rising at a 0.1% pace

the previous period. Output

advanced at a 0.4% rate, the weakest in 2 years, following a

1.5% pace. Total hours worked eased to a 1.5% rate from

3.3% in Q4. Growth

slowed to a crawl in Q1 as

consumers & companies alike reined in their spending amid weak global

financial conditions & a plunge in oil prices. When that

environment is combined with the uncertainty accompanying the election

season, the much-needed pickup in business investment may remain

elusive. That, in turn, doesn't bode well for workers’ wages as

companies strive to protect profits.

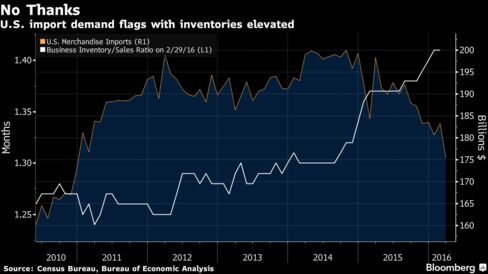

America's trade deficit shrank more than forecast in Mar as imports

fell in percentage terms by the most in 7 years & outpaced a

decline in shipments overseas. The gap narrowed 13.9% to

$40.4B, the smallest since Feb 2015, according to the Commerce Dept. The forecast was

for a $41.2B deficit. Imported merchandise declined 3.6%, the most since Feb 2009, as American companies worked to

get inventories in line with weaker Q1 demand. At the same

time, shipments overseas fell for the 5th time in 6 months amid soft

global sales. After eliminating the effects

of price fluctuations, which generates numbers used to calculate

GDP, the trade deficit narrowed to $57.4B from $63.2B a month earlier. The Mar real trade gap was the

smallest since Jul. The

initial estimate showed trade subtracted 0.34

percentage point from Q1 GDP when the economy expanded an

annualized 0.5%. Trade has contributed to growth in just one

qtr out of the last 6. Imports decreased to $217B, the smallest since Feb 2011, from $225B a month

earlier. The slump in purchases from overseas was broad-based &

included capital equipment, consumer goods & industrial supplies such

as oil.

The petroleum deficit narrowed to $3B, the smallest since 1999. Exports

decreased 0.9% to $176.6B from $178.2B

the prior month. Middling overseas demand hobbled orders for consumer

goods, which declined to a 3-year low. Exports of industrial

supplies were the weakest since Feb 2010.

American service companies expanded in Apr at the fastest pace in 4 months, signaling the economy is firming up after a weak start to

the year. The Institute for Supply Management non-manufacturing index rose to

55.7 from 54.5 in Mar. Readings above 50 signal growth. The forecast called for 54.8. The improvement shows service producers, which account for almost 90% of the economy, gained some traction following the slowest

quarterly growth pace in 2 years. Industries including retailers,

builders & health-care providers have been less vulnerable to weakness

overseas that’s kept pressure on US factories. The measure averaged 53.8 this year thru Mar, compared with

57.2 in all of 2015. The new orders gauge climbed to a 6-month high of 59.9

from 56.7 the prior month & the measure of services employment rose to 53

from 50.3. The business activity index, which parallels the ISM's factory

production gauge, eased by 1 point to 58.8 last month. A measure of

prices paid jumped to 53.4, the highest since May 2015 & indicating

costs were accelerating, from 49.1 the prior month. The supplier deliveries gauge, which

measures how quickly companies are able to process orders, held at 51.

Readings above 50 mean delivery times slowed, which is a positive signal

as it indicates companies were having a bit more trouble keeping pace

with demand.

Not much going on in the stock market. OPEC is looking to see if it can set production quotas next month & oil rallied. Don't hold your breath on that. Dow remains within 500 of setting a record high even though economic fundamentals are nothing to write home about.

No comments:

Post a Comment