Dow dropped 56, decliners over advancers 4-3 & NAZ gave up 29. The MLP index rose 2+ to the 294s & the REIT index is back in the 334s where is has been for more than a month. Junk bond funds were a little higher & Treasuries rallied. Oil slid back pennies to 47 (see below) & gold shot up again, pushing towards 1300.

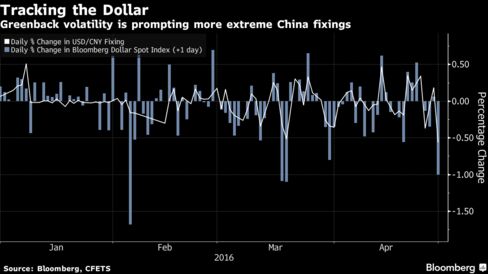

China's central bank responded to an overnight tumble in the $ by

strengthening its currency fixing the most since a peg was dismantled in

Jul 2005. The reference rate was raised 0.6% to 6.4589 per $. A

gauge of the $'s strength extended its 1% slide yesterday,

when the Bank of Japan's decision to unexpectedly keep monetary policy

unchanged sent the ¥ surging. While the

change in the fixing is extreme relative to the small moves of recent

years, it reflects increased volatility in the $

against other major exchange rates rather than a policy shift by the

People's Bank of China.

The $ headed for its the lowest close in almost a year today as

signs of slowing growth in the US dimmed prospects for a Federal

Reserve interest-rate increase.

Caterpillar, a Dow stock, will close 5 US plants & shed

820 positions as the construction-equipment maker continues to

scale back its production & workforce in response to falling demand.

The cutbacks are part of a strategy outlined in Sep to trim its workforce by 10K &

close or consolidate about 20 facilities thru 2018. The company said

it has shed about 5.3K positions so far. The plants designated

for closure mostly produce components for its machinery &

engines & their operations will be merged into other plants

or assigned to parts suppliers outside of the company during the next 12-18 months. CAT has a world-wide workforce of 114K. 2016 revenue is expected to be down about 38% from

the peak level of $66B in 2012, as the company

struggles through a global sales slump for mining & construction

machinery. The stock slid back pennies. If you would like to learn more about CAT, click on this link: club.ino.com/trend/analysis/stock/CAT?a_aid=CD3289&a_bid=6ae5b6f7

Oil pared its loss after data from Baker Hughes showed that the number if active US rigs drilling for crude fell 11 to 332, down for a 6th

straight week. Total US rig count fell 11 to 420.

After posting its first quarterly loss in 14 years last quarter, Chevron (a Dow stock) wasn't able to turn things around to get much better

results. The loss per share was 39¢, a

reflection of how brutal the oil & gas market has been.

Chevron's results: The raw numbers

Metric

Q1 2016

Q4 2015

Q1 2015

Revenue

$23.553 billion

$29.247 billion

$34.558 billion

EBITDA

$2.692 billion

$4.290 billion

$7.316 billion

Net income

($725 million)

($588 million)

$2.567 billion

Earnings per share

($0.39)

($0.31)

$1.38

The 2 big pain points were commodity

prices & weaker refining margins. Beyond that, the company wasn't able

to offset those issues with upticks in production or refinery

throughput. In Q1, the average realized price for a

barrel of oil was only $28, compared to $44 last year. Even

with drastic cuts to the cost structure, it's close to

impossible to make a profit at that price point. The

company reduced capital & exploratory spending by 19% compared to

last year as some major capital projects have come online, but cash flow

from operations has dried up even faster. Not only did CVX need to

take out another $3.8B in debt, but it also had to reach into its

cash pile to pay the rest of its expenses. The company said that it is doing everything

that it can to preserve its financial standing while paying out a

div. It expects that, by 2017, it will be able to

cover all capital expenses & divs with operational cash flow, &

Brent crude oil at $52. It believes it can achieve this by reducing

capital & exploratory spending by $15B from 2015 levels. The stock also lost just pennies. If you would like to learn more about CVX, click on this link: club.ino.com/trend/analysis/stock/CVX?a_aid=CD3289&a_bid=6ae5b6f7

The stock market tried to extend its gains after the Dow went up more than 2K in 2 months. But it stalled out. The weak $ is causing problems & earnings on balance have not been a help. Drab growth for GDP in Q1 announced today is another negative. Dow managed to gain of less than 100 in Apr.

Dow dropped 76, decliners a little ahead of advancers & NAZ was off 28. The MLP index lost pennies in the 294s & the REIT index is in the 334s (trading in a tight range for weeks). Junk bond funds fluctuated & Treasuries retreated. Oil & gold rallied again.

Consumer spending rose less than forecast in Mar, wrapping up the

weakest qtr in a year for the biggest part of the US economy even

as incomes accelerated. Purchases picked up 0.1% after a

revised 0.2% gain in Feb, according to the Commerce Dept. The forecast called for a 0.2% advance. Incomes increased 0.4%, matching Jan as the

biggest gain since Jun. A tempering of household purchases for

the last 3 qtrs has been surprising given the favorable

backdrop of low inflation, job gains & cheap borrowing costs. Faster

wage growth may be needed to help encourage American consumers to spend

more freely & jump start an economy coming off its weakest performance

in 2 years

Disposable

income, money left over after taxes, increased 0.3% in Mar

from the prior month after adjusting for inflation following a 0.2% gain in Feb. The

saving rate rose to 5.4% last month, the highest in more than a

year. At $735B, the level of savings was the highest since

Dec 2012. In Q1, real disposable income rose

at a 2.9% annualized rate after a 2.3% pace in Q4-2015. In Q1-2015, it was running

at a 3.9% clip. Wages & salaries climbed at a 3.9% pace in Q1, the slowest pace in a year. The price index tied to consumer spending increased 0.1% last month after falling 0.1% in Feb. From a year

earlier, the gauge was up 0.8%. This inflation measure is

preferred by Federal Reserve policy makers & it hasn't met their

target since Apr 2012. Stripping out the volatile food &

energy components, the price measure also rose 0.1% from the

month before & 1.6% in the 12 months ended Mar.

Consumer confidence fell to a 7-month low in Apr as Americans'

expectations about economic growth dropped to the lowest point since

Sep 2014. The University of Michigan final index of sentiment declined to 89

from 91 in Mar. The projection was 90 & the preliminary reading for this month was 89.7. Worker pay that’s advanced slowly during the expansion & the

ongoing negativity in the presidential election campaign have left

Americans guarded. While households viewed their finances as currently

favorable, they're saving more in the event that employment softens

along with wage growth. “The top concerns of consumers involve whether the slowdown in

economic growth will result in a slower pace of income and job gains,

and growing uncertainty about future economic policies depending on the

outcome of the presidential election,” the

Univ of Michigan consumer survey said. “On both

counts, consumers have already adopted a more defensive stance.”

The gauge averaged 92.9 last year, the best annual performance since

2004. The sentiment report's measure of expectations 6 months from now decreased to 77.6 from 81.5. For the year ahead, respondents anticipated income gains of 1.2%, the smallest in the past year. More also expected the unemployment rate to increase. “When asked to identify what economic

news they had recently heard, negative references to the election and

government policies rose to 18 percent in April, up from 10 percent last

month,” according to the survey. The current conditions index, which takes stock of Americans’ view of

their personal finances, rose to 106.7 from the prior month’s 105.6. Consumers projected the inflation rate in the next year will be 2.8%, up from 2.7% in the Mar survey. Over the next 5-10 years, they expect a 2.5% rate of inflation, matching the

lowest in records to 1979. It was 2.7% the previous month. Other recent reports on household confidence have been mixed.

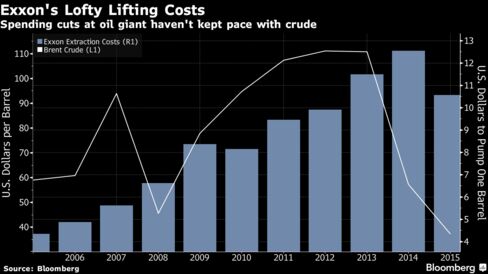

Exxon Mobil, a Dow stock & Dividend Aristocrat, beat lowered estimates as a jump in earnings from

its chemicals segment cushioned the blow from tumbling prices for oil & natural gas. Q1 EPS fell to 43¢ from $1.17 a year earlier. The quarterly profit was the lowest in 17 years. Still, EPS was 15¢ above

estimate. Results were boosted by a 38% increase in its petrochemicals division, to $1.4B, as

well as a 33% cut in capital expenditures as it pulled back on

drilling & exploration amid weak commodity prices. The

chemicals division benefited from stronger margins & higher sales

volumes, as the price of raw materials plunged

compared to last year's Q1. The downstream segment earned

$906M as global gasoline demand remained strong. The 2016 capital budget has been

cut 33% from last year, a bigger decline than earlier

estimated. Despite those measures, full-year EPS is expected to dip

below $10B in 2016 for the first time since 1999.

“The organization continues to respond

effectively to challenging industry conditions, capturing enhancements

to operational performance and creating margin uplift despite low

prices,” CEO Rex W. Tillerson said. “The scale and integrated nature of our cash flow provide

competitive advantage and support consistent strategy execution.” The stock rose 82¢. If you would like to learn more about XOM, click on this link: club.ino.com/trend/analysis/stock/XOM?a_aid=CD3289&a_bid=6ae5b6f7

Once again, economic & earnings news stories are unexciting. The strength of the US economy is far less than robust, & this is one of the strongest economies in the world. The weak $ is helping oil to advance, but that does not have spillover effects in other markets. As has been the case for almost a decade, the US consumer keeps showing inconsistent patterns of spending. The economy is not as strong as some indicate. However, Dow is up YTD to about 500 below the record highs last year.

![Live 24 hours gold chart [Kitco Inc.]](http://www.kitco.com/images/live/gold.gif?0.522439727495085)