This blog gives investors more financial information for very smart investing!

Thursday, April 14, 2016

Markets little changed ahead of Doha oil meeting

Dow added 18, decliners over advancers 5-4 & NAZ was off 1. The MLP index slid back 1+ to the 276s & the REIT index was up fractionally in the 337s. Junk bond funds were higher & Treasuries drifted lower. Oil was lower in late day trading (see below) & gold also retreated.

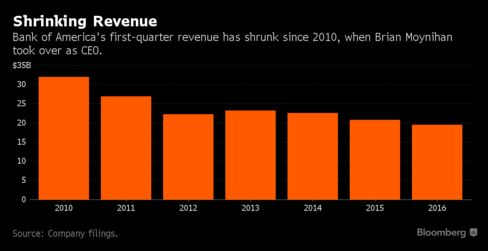

Bank of America Q1 profit missed

estimates as trading & underwriting revenue dropped &

energy loans soured. EPS fell to 21¢ from 25¢ , a year earlier. Adjusted EPS was 20¢, a penny less than the estimate.

CEO Brian T. Moynihan spent the first half-decade of

his tenure wrestling with legal costs tied to his predecessor’s

acquisitions of Countrywide Financial & Merrill Lynch.

His attempt to bolster revenue has been hamstrung by low interest rates & rising costs from energy loans that went bad as oil prices plunged. “In

quarters like this, revenue is going to be challenged,” CFO Paul Donofrio said.

“Markets were volatile, and long-term interest rates declined

significantly.” Revenue

fell 6.7% to $19.5B, missing the $20.4B estimate. Expenses declined 6.4% to

$14.8B, below the $15.1B predicted. Profit

from the global-markets division fell 4% to $889M, excluding the impact of accounting adjustments tied to debt

valuations. Adjusted revenue from trading fell 16% to $3.3B, driven by declines in bond & stock transactions. That

compares with the $3.29B estimate. A tough

environment for credit trading contributed to a 17% drop in

fixed-income revenue to $2.26B, shy of the $2.32B

estimate. Equities trading

declined 11% to $1.02B, missing the $1.15B

estimate. The global-banking division posted a 22M profit

decline to $1.07B, on a similar drop in investment-banking fees.

That compares with the $1.3B estimate. The company more than doubled the amount it set aside for soured energy

loans, boosting it by $525M from the end of last year to $1B as of Mar 31, driven by its exposure to the

exploration-and-production & oil-field-services industries. At the

same time, the bank reduced the number of outstanding energy-related

loans by $325M from a year earlier. The stock rallied & went up 35¢. If you would like to learn more about BAC, click on this link:lub.ino.com/trend/analysis/stock/BAC?a_aid=CD3289&a_bid=6ae5b6f7

Wells Fargo, the top oil & gas banker, Q1 profit fell as it set aside more money

for soured energy loans & expenses increased. EPS was 99¢, down from $1.04 a year

earlier. But that beat the 97¢ estimate.

CEO John Stumpf has sought to keep expenses in check,

while increasing deposits & expanding the loan portfolio with

strategic acquisitions. “While

challenges in the energy industry and persistent low rates impacted our

bottom line, our diversified business model was again beneficial to our

results,” CFO John Shrewsberry said. Revenue

climbed 3.8% to $22.2B, beating

estimates of $21.6B. Net interest income rose 6.2% to $11.7B, while expenses increased 4.2% to $13B on higher employee benefits & incentive compensation. Net

interest margin, a measure of profitability, declined 5 basis points

from the previous qtr to 2.90%. The firm set aside

$1.09B for bad loans, a 79% increase from a year earlier,

fueled largely by exposure to the oil & gas industry. It

reserved $1.7B to cover potential losses on energy loans, up $500M from the end of 2015. The bank had $17.8B in

outstanding loans to the industry at the end of Q1 (1.9% of its portfolio). Profit

in the community-banking division, which houses the

branch-based business as well as mortgage & credit-card lending,

declined 7.1% from a year earlier to $3.3B. Net income in

wholesale banking, which includes the commercial real estate business

and securities unit, fell 2.7% to $1.92B. Wealth &

investment-management posted profit of $512M, a 3.2% drop. The

bank’s efficiency ratio, a measure of how much it costs to generate a $ of revenue, fell to 58.7%, near the upper end of the

firm's target range. The stock was down 24¢. If you would like to learn more about WFC, click on this link: lub.ino.com/trend/analysis/stock/WFC?a_aid=CD3289&a_bid=6ae5b6f7

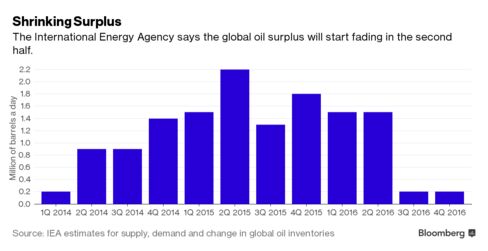

Oil was flattish before a meeting of major producers this weekend as the

International Energy Agency predicted that global oversupply will almost

vanish in H2. Global oil markets will “move close

to balance” as lower prices take their toll on output outside OPEC, the

IEA said. Qatar said it has a “positive feeling” about

the Apr 17 talks in Doha aimed at agreeing on a production freeze.

While 40 analysts & traders

surveyed were evenly split over whether the Doha talks will

succeed, a majority of those who predicted a deal said it would have no

impact on actual flows of crude. The world surplus will diminish to 200K barrels a day in H2 from 1.5M in H1, the IEA said. Production

outside OPEC will decline

by the most since 1992 as the US shale-oil boom falters.

Little is going on in the early days of earnings season. The first reports are glum, although traders are putting a positive spin on the numbers. Next week there will more reports & they will not be pretty. The big oil meeting this weekend aimed at limiting production probably will be a non-event. This ad-hoc group of producers with different agendas can not be counted onto agree to anything. Even the bullish sentiment which has been driving oil prices higher is taking a rest. Meanwhile, the stock market is VASTLY overbought.

![Live 24 hours gold chart [Kitco Inc.]](http://www.kitco.com/images/live/gold.gif?0.385668584159226)

No comments:

Post a Comment