This blog gives investors more financial information for very smart investing!

Thursday, June 23, 2016

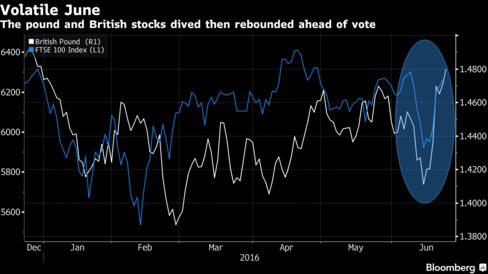

Markets rise as polls show Britain will stay in the EU

Dow gained 129, advancers over decliners a big 5-1 & NAZ gained 37. The MLP index went up 1+ to the 317s & the REIT index added 1+ to 351, closing in on its record high. Junk bond funds rose & Treasuries retreated. Oil joined in the rally for commodities while safe haven gold pulled back.

Stocks gained & the £ strengthened to its highest level this

year as the last 2 polls showed a lead for the

campaign to keep Britain in the EU. Euro shares

rose to the highest level in more than 2 weeks in above-average

trading with voting underway in the UK's referendum. The S&P 500

climbed within 1½% of its all-time high. Gold & the ¥ declined, while perceived corp

credit risk fell for a 5th day. In 2 opinion polls conducted

Jun 21-22, the “Remain” camp was shown to be in front.

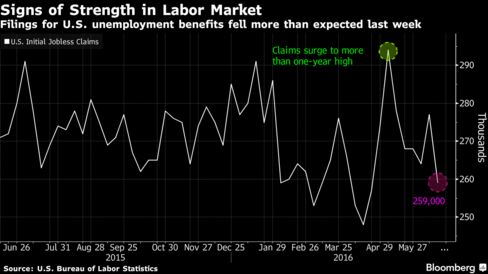

Fewer Americans than forecast filed for unemployment benefits last

week, adding to evidence that the labor market is healthy & stable. Jobless

claims dropped by 18K to 259K, according to the

Labor Dept. It was the biggest decrease

since the early Feb. The forecast called for a decline to 270K.

Hiring

managers are finding little reason to pare staff amid a dwindling pool

of available workers. Sustained low levels of jobless claims have helped

to reassure the Federal Reserve that the recent slowdown in

payroll gains will dissipate. Filings

have been below 300K for 68 straight weeks, the longest stretch

since 1973, & a level consistent with a

healthy labor market. The 4-week average of claims, a less-volatile measure than the weekly

figure, fell to 267K from 269K in the prior week. Last week

included the 12th of the month, which coincides with the period the

Labor Dept surveys employers to calculate monthly payroll data.

The average is lower than the 278K during the comparable period in

May. The number continuing to receive jobless benefits

decreased 20K to 2.14M & the

unemployment rate among people eligible for benefits held at 1.6%.

Purchases of new homes declined in May from an 8-year high as the

housing market continued to display the choppy progress that’s been a

hallmark of the recovery. Sales fell 6% to a 551K

annualized pace following a 586K rate in Apr that was slower than

previously estimated, from the Commerce Dept. The estimate was for a 560K. While

the report showed demand retrenched last month, the volatile data are

showing gradual improvement on the back of steady job gains & low

mortgage rates. Stronger wage growth & a greater availability of

cheaper properties would help lure more first-time buyers & provide an

additional push for the housing recovery. Because new-home sales figures for the 3 previous

months were revised lower, the May data should also be considered

preliminary. Over the last 3 months, purchases have averaged a

553K pace, the best in 8 years.

New-home

purchases were 8.6% higher in May from a year earlier on an

unadjusted basis. 201K homes sold in May weren't yet started by builders, the most

since Jun 2007, indicating construction starts may firm up in the

months ahead, & help drive economic growth. Purchases fell in 3 of 4 regions, led by a 33.3% decrease in the

Northeast (the smallest market for new homes). The supply of homes at the current sales rate increased to

5.3 months from 4.9 months in Apr. There were 244K new houses on

the market at the end of last month, up from 241K & the most since

Sep 2009. The median price of a new home increased 1% last month from a year ago to $290K.

Stocks are in rally mode as indications are that Britain will remain in the EU. When that matter is settled, markets will watch fundamentals. This week oil has bounced back from recent selling, but it continues to be highly volatile.

No comments:

Post a Comment