This blog gives investors more financial information for very smart investing!

Wednesday, June 1, 2016

Month starts with lower markets on manufacturing data

Dow dropped 81, decliners over advancers 4-3 & NAZ lost 8. The MLP index rose 1+ to 304 & the REIT index was flattish at 341. Junk bond funds crawled higher & Treasuries were a little higher. Oil sold off & gold was also weak.

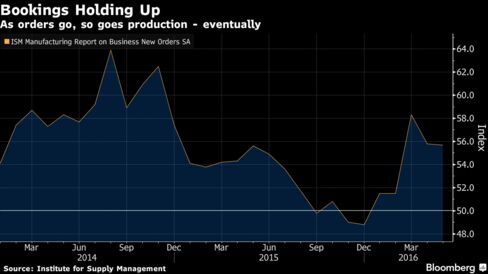

Manufacturing unexpectedly expanded at a faster pace in May, helped

by an increase in orders that signals US factories are rebounding from

an early-2016 slump. The Institute for Supply Management index

climbed to 51.3 from 50.8 in Apr. The forecast called for 50.3. Readings greater than 50

indicate growth.

Factories

are using a pickup in bookings from the US & abroad to help trim

stockpiles, laying the ground for bigger gains in production later in

the year. The recent pickup in oil prices also will probably help stem

the slump among energy producers that has contributed to weak business

investment. The new orders gauge was little changed at 55.7 compared with 55.8 in Apr while the measure of production cooled to 52.6 from 54.2. One weak spot was the factory employment measure, which held at 49.2, indicating manufacturers trimmed payrolls last month. In

other signs that the industry is turning around, the index of supplier

deliveries jumped to 54.1, the highest level since Dec, from

49.1. A reading greater than 50 means shipments slowed, which often

happens when suppliers have trouble keeping up with demand. The

gauge of factory inventories fell to 45 from 45.5. The index has

been lower than 50 for almost a year as producers trim goods on hand. The report also showed the headwind from sluggish

overseas markets may be dissipating. The index of export orders held at

52.5, marking the 3rd straight month demand from abroad has

grown.

General Motors (GM) & Ford (F) US vehicle sales fell in May more

than had been estimated, raising questions about stalling

consumer demand. GM sales plunged 18%, missing estimates

for a 13% drop, with all 4 brands reporting declines of at

least 14%. Ford's light-vehicle sales slid 6.1%, compared with an estimate for a 4.9%

decline. GM projects a sales pace for the month that is slower than had predicted. All of the 6 largest carmakers were

estimated to report declines for May. Even as auto sales gained in Apr & the US consumer continues to spend,

there have been signs of wavering economic confidence, & the industry

may struggle to maintain its record pace. As a kickoff into summer on

the back of Memorial Day weekend promotions, May is a bellwether for

gauging buyer appetite.

GM projected the sales pace,

adjusted for seasonal trends, will be 17M, short of the estimate for a 17.4M rate for the month.

China stocks dipped following the previous day's sharp

rally, as growing optimism about MSCI adding mainland stocks to its

emerging markets index was offset by worries over China's economy & a

looming US rate hike. The blue-chip CSI300 index fell 0.3%, to 3160, while

the Shanghai Composite Index dipped 0.1%, to 2913. There was little market reaction to the official & private

surveys on China's manufacturing activity, which were roughly in line

with expectations, underlining doubts that the world's 2nd-largest

economy is picking up. Some investors took profit from yesterday's more than 3%, which was underpinned by expectations that US

market index provider MSCI could add mainland stocks to its emerging

market benchmark for the first time.

Even though stock markets did not do much in May, stocks remain overbought after its rise from the Feb lows. US economic data continues to be uneven, but it may be just good enough (shown by manufacturing data) to justify a rate hike in 2 weeks. That worries traders who are addicted to low interest rates.

No comments:

Post a Comment