This blog gives investors more financial information for very smart investing!

Tuesday, August 9, 2016

Higher markets with Nasdaq reaching a new record high

Dow went up 43, advancers over decliners almost 3-2 & NAZ added 20. The MLP index lost pennies in the 317s & the REIT index was up a fraction to the 369s. Junk bond funds edged higher & Treasuries rose. Oil slid lower & gold found buyers.

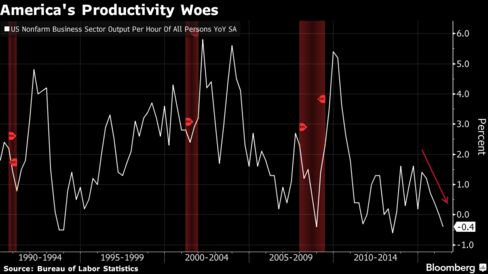

The productivity of American workers unexpectedly declined for a 3rd straight qtr, deepening efficiency woes that have

characterized the economic expansion. The measure of employee

output per hour decreased at a 0.5% annualized rate in Q2 after dropping 0.6% in the prior qtr, according to the Labor Dept. The

forecast called for a 0.4% gain. Expenses

per worker climbed at a 2% pace after being revised to a decline

in the previous period. Productivity compared with a year earlier

fell for the first time since 2013 as lackluster global markets prompted

companies to scale back capital investment plans. In the face of

deteriorating corporate profits & an absence of faster economic

growth, the risk is that businesses may begin to ratchet back the hiring

they’ve relied on to meet demand. Unit

labor costs, which are adjusted for efficiency gains, were forecast to

increase 1.8% in Q2. In the prior qtr, they were revised to a 0.2%

decrease from an initially reported 4.5% advance. Adjusted

for inflation, hourly compensation fell at a 1.1% rate, the most in 2 years, after dropping 0.4% in Q1. Worker efficiency fell 0.4% from the same time in 2015, while labor costs climbed 2.1%.

The Q2 reading on productivity compares with the 2.6% average over 2000-2007. Among manufacturers, productivity declined at a 0.2% rate after a 1.5% gain in Q1. Growth

continued to disappoint in Q1. Amid

fragile global growth prospects & presidential election year

uncertainty, the risk is that business investment continues to languish.

That may bode ill for workers, whose potential for wage increases

could suffer as companies look to get the most out of weak profits.

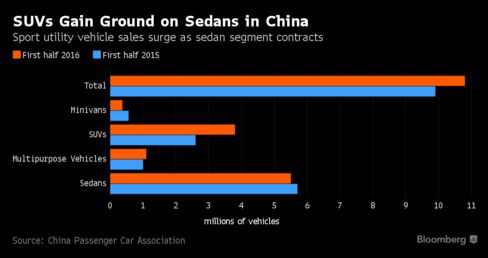

China’s passenger-vehicle sales accelerated the most in 17 months, as

General Motors (GM) & Guangzhou Automobile boosted

deliveries & dealers offering discounts helped clear inventories in

the world’s biggest auto market. Retail sales of cars, sport

utility & multipurpose vehicles climbed 23% to 1.6M

units in Jul, the biggest monthly percentage gain since Feb 2015,

according to the China Passenger Car Association. Deliveries increased

to 12.4M units in the 7 months thru Jul. Dealers offered discounts on models to help reduce stockpiles. A gauge of inventory levels fell

to an 11-month low & indicated contraction for the first time in that

span, the China Automobile Dealer Association said.

The

gov's purchase-tax cut on vehicles with smaller engines has

helped drive demand for compact & mid-size SUVs. With increasingly

affluent Chinese buyers opting for more spacious vehicles, SUVs sales

grew 45% in Jul, outpacing the 15% expansion for sedan

models. Deliveries for GM increased 18%

to 270K units, while Ford (F) rose 15% to

88K vehicles. Toyota (TM) sales gained 5.7% to 97K

units.

US wholesale inventories unexpectedly rose in Jun on gains in

stocks of farm products & other nondurable goods, suggesting an upward

revision to Q2 economic growth estimate. The Commerce Dept said that wholesale

inventories increased 0.3% after having been initially estimated

as unchanged. Inventories for May were revised up to show a 0.2%

rise instead of the previously reported 0.1% gain. The forecast for wholesale inventories was for unchanged in

Jun in line with the gov estimate last month. That unchanged

reading was incorporated in the advance Q2 GDP estimate. The component of wholesale inventories that goes into the

calculation of GDP, wholesale stocks excluding autos, increased 0.3% in Jun. That would imply a mild upward revision to the

Q2 GDP growth estimate. An outright drop in inventory investment subtracted almost 1.2

percentage points from GDP growth in Q2, restricting the

rise in output to a tepid 1.2% annualized rate.

The sellers are away at the beach, enjoying the warm weather, the buyers are in command of the stock market. News continues to be more of the same & the path of least resistance for stocks is to head north. But the dark clouds of uncertainty have not gone away.

No comments:

Post a Comment