This blog gives investors more financial information for very smart investing!

Thursday, August 4, 2016

Markets drift lower after factory orders report

Dow fell 4, advancers over decliners 4-3 & NAZ gained 8. The MLP index was off 6+ to 310 & the REIT index lost 1 to the 368s. Junk bond funds were a little higher & Treasuries rose. Oil was a little lower & gold was bid higher

Mark Carney unleashed a package of stimulus, including the Bank of

England's first interest-rate cut in 7 years, & said more easing

could come as Britain feels the effects of its decision to leave the

EU. Officials voted

unanimously to reduce the benchmark by 25 basis points to a record-low

0.25%. They split over other elements of the plan that will

expand the central bank’s balance sheet by as much as £170M

($223M) via purchases of gilts & corp bonds & a lending

program for banks. “We took these steps because the economic outlook has changed markedly,”

Carney said. “Indicators have all

fallen sharply, in most cases to levels last seen in the financial

crisis, and in some cases to all-time lows.” Policy makers slashed growth forecasts by the most ever & Carney

declared that all elements of the stimulus can be taken further,

including another rate cut. The Monetary Policy Committee's measures

include a plan to buy £60B of gov bonds over 6

months, as much as £10B of corp bonds in the next 18

months & a potential £100B loan program for banks. Should

their outlook for the economy prove correct, “a majority of members

expect to support a further cut in bank rate to its effective lower

bound” later this year, they said. Carney said multiple

times that this doesn’t mean rates will be negative. “The MPC is

very clear that we see effective lower bound as a positive number, close

to zero, but a positive number,” he added. “I’m not a fan of negative

interest rates,” he said, noting that they had produced “negative

consequences” elsewhere.

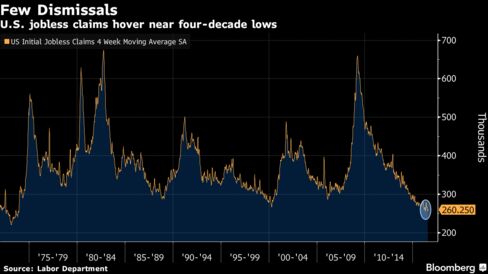

The number of Americans filing applications for unemployment benefits

rose last week to a level that still underscores health in the labor

market. Jobless claims rose 3K to 269K in the latest week, according to the Labor Dept. The forecast called for

265K. Continuing claims decreased. A limited number of layoffs

indicates companies are retaining employees at a time when skilled &

experienced workers are in greater demand. Further improvement in the

job market will be critical in helping drive consumer spending, the

biggest part of the economy, during H2. For 74 consecutive weeks, claims have been below the

300K, a level that is consistent with an

improving job market (the longest stretch since 1973). The 4-week moving average increased to 260K

last week after falling to 256K in the previous period (the 2nd-lowest level since 1973).

The

number continuing to receive jobless benefits dropped 6K to 2.14M & the unemployment rate

among people eligible for benefits held at 1.6%.

New orders for US factory goods fell for a 2nd straight month in

Jun on weak demand for transportation equipment & capital goods, but

signs of stabilization in business spending offered some hope for

struggling industries. The Commerce Dept said that new orders for

manufactured goods declined 1.5% after a downwardly revised 1.2% decrease in May. The forecast for factory orders called for the figure to drop

1.8% after a previously reported 1.0% decline in

May. Core capital goods shipments, which are used to calculate

business equipment spending in the GDP report, fell

0.2% in Jun. Manufacturing, which accounts for about 12% of the

economy, has been pressured by the residual effects of a strong $ & a weak global demand, which have undermined exports of factory goods.

Production has also been hurt by businesses placing fewer orders as they

try to clear an inventory glut. The sector has also been hurt by spending cuts by energy firms as they adjust to reduced profits from cheaper oil. An outright drop in inventories & sustained weakness in

business spending weighed on economic growth in Q2, with

GDP rising at a tepid 1.2% annualized rate. In Jun, orders for transportation equipment tumbled 10.5%, the biggest drop since Aug 2014. That largely reflected weak

orders for aircraft. Orders for motor vehicles & parts increased 3.2%, the largest gain since July 2015. Orders for machinery, which have been hurt by weak demand in the

energy & agricultural sectors, rose 0.2%. Orders for electrical

equipment, appliances & components gained 0.3%. Orders for

computers & electronic products slumped 1.9%, the largest drop

in more than a year. Inventories of factory goods dipped 0.1%. Inventories have

declined in 13 of the last 14 months. Shipments increased 0.7%, lowering the inventories-to-shipments ratio to 1.35 from 1.36 in

May. Unfilled orders at factories decreased 0.8% after 3 straight months of increases.

Stocks are not doing very much as traders wait for the Jul jobs report tomorrow. Dow is down slightly in Aug & still looks like it will be heading lower this month without positive news to bring out buyers.

No comments:

Post a Comment