This blog gives investors more financial information for very smart investing!

Wednesday, August 31, 2016

Lower markets on August employee data

Dow dropped 40, decliners over advancers 4-3 & NAZ fell 10. The MLP index lost 2+ to the 308s & the REIT index was fractionally lower in the 361s. Junk bond funds were little changed & Treasuries crawled higher. Oil & gold were each lower again.

Euro-area inflation failed to accelerate in Aug, adding to signs

that the area's economic outlook deteriorated ahead of a ECB meeting next week. Consumer prices rose 0.2%

in Aug from a year earlier. The estimate

was for an increase of 0.3%. 2 months after the UK

Brexit vote, the 19-nation economy is beginning to show signs of

faltering, suggesting that more stimulus may be warranted. Business &

consumer sentiment declined & executives are warning that orders may

suffer from political uncertainty. The IMF has

already cut its forecast for euro-area growth next year & the

ECB will release new projections after its meeting

next week. Policy

makers have already deployed a raft of unconventional stimulus that

includes large-scale asset purchases, negative interest rates &

long-term loans that see banks getting paid for extending credit to

companies & households. Still, inflation remains far below the ECB

goal of just under 2%, a level it hasn't reached since early

2013. The institution predicts price growth will accelerate to 1.6% in 2018. Core

inflation slowed to 0.8% from 0.9% a month

earlier. German inflation unexpectedly decelerated to 0.3%, while consumer prices extended their decline in Spain. Euro-area unemployment remained unchanged at 10.1%, according to a separate release. The inflation report comes one day after a European Commission survey

showed economic confidence declined across most countries & most

sectors in a delayed reaction to Britain's decision to leave the

EU. The data may reopen the debate about more stimulus at

the ECB's Sep 8 meeting.

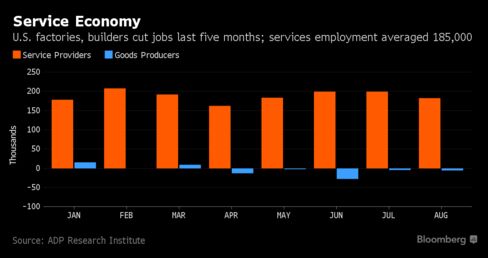

Companies added workers to US payrolls in Aug in line with

projections, contributing to signs of a steady labor market, data from

ADP Research Institute. Private

payrolls climbed 177K (forecast was 175,K) after a revised

194K gain in Jul (more than initially estimated). Goods-producing industries, which include manufacturers & builders, reduced headcounts by 6K. Service providers’ payrolls rose 183K. Hiring managers are taking on workers to meet sales, evidence of

sustained job-market progress that Federal Reserve officials will weigh

when they meet in Sep.

“The

American job machine continues to hum along,” Mark Zandi, chief

economist at Moody’s Analytics said. “Job creation remains strong, with most industries and

companies of all sizes adding solidly to their payrolls. The U.S.

economy will soon be at full employment.” Moody's produces the figures

with ADP. Companies

employing 500 or more workers increased staffing by 70K jobs;

payrolls rose by 44K at medium-sized businesses (those with 50-499 employees) while small companies' payrolls advanced 63K.

The Institute for Supply Management's gauge of factory activity in the

Midwest region fell to 51.5 in Aug from 55.8 the month prior. The forecast was for a smaller decline to a reading of 54.0. Readings above

50 point to expansion, while those below indicate contraction.

Not much going on today in the slowest week of the year. Stock averages have been trading sideways for most of the summer & that trend should not change until after Labor Day (at the earliest). Oil tried to rally, hoping to top 50, but that effort failed. Gold is sliding lower from the mid 1300s to the low 1300s.

No comments:

Post a Comment