This blog gives investors more financial information for very smart investing!

Friday, August 12, 2016

Markets fluctuate on consumer confidence data

Dow pulled back 37 decliners slightly over advancers & NAZ added 4. The MLP index advanced 2+ to the 315s & the REIT index went up 1+ to the 367s. Junk bond funds did little & Treasuries rallied, taking the yield on the 10 year Treasury near 1½%. Oil went up 1 to the 48s while gold finished the day lower.

Investors pulled $32.9B last month from actively managed US

mutual funds that buy domestic stocks in Jul, the biggest monthly

outflow in data going back to 1993, as money continues to move into

low-cost passively managed funds, according to Morningstar. About

an equal amount, $33.8B, went into passive funds that invest in

US equities. US-based

active funds that buy domestic equities had redemptions of $211B

in the 12 months thru Jul while investors poured $163.6B

into passively managed funds during the period as active managers failed

to generate returns above indexes that justify their higher fees. Almost $401B has flowed into passively managed mutual funds &

exchange traded-funds over the past year as $327.8B was withdrawn

from actively-managed funds. Passively-managed funds now oversee

about 43% of equity funds & 28% of taxable

bonds.

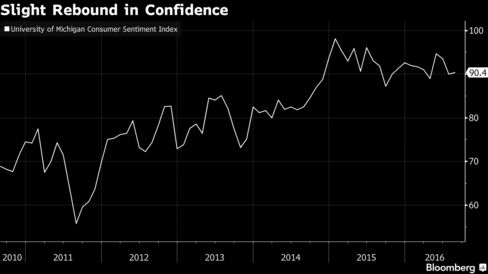

Consumer confidence in the US rose less than forecast in Aug,

reflecting a pullback in views on personal finances among younger

Americans. The Univ of Michigan’s preliminary index of

sentiment climbed to 90.4 from a 3-month low of 90 in Jul. The projection called for a reading of 91.5. Payrolls have shown strong gains for 2 months & wage

increases are slowly accelerating, giving consumers more confidence and

power to spend. At the same time, uncertainty over the outcome of the

presidential election could hold back the household demand that's

supported economic growth this year amid weak investment by companies.

Increasing

uncertainty about the economy following the election “probably reflects

each candidate’s focus on the negative economic outcomes if the other

candidate is elected,” Richard Curtin, director of the survey, said. The Michigan current conditions

index, which is an assessment of the state of personal finances,

declined to a 5-month low of 106.1 from 109 in Jul & a gauge of

expectations for the next 6 months rebounded to 80.3 from 77.8 last

month. Inflation expectations for the next

year were at 2.5%, a 3-month low, compared to 2.7% in

Jul. Over the next 5-10 years, Americans expected prices to rise

2.6%, unchanged from the prior month, & just above the record

low of 2.5%. The

index of current personal finances dropped to a 4-month low of 119

from 121. Only 30% of respondents expected their incomes

to improve over the next year, the lowest since late 2014, with the

latest decline coming among those under age 45.

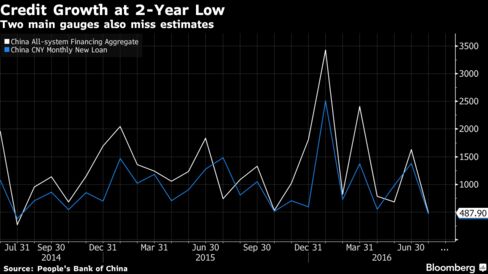

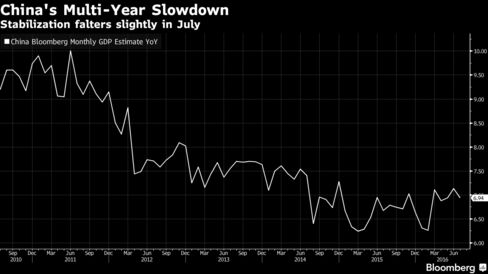

China's recent economic stabilization faltered in Jul as factory

output, retail sales & investment all slowed, while the broadest

measure of new credit rose the least in 2 years. All main indicators missed estimates:

Industrial production rose 6% in Jul from a year earlier, less than the projected 6.2% gain

Retail sales climbed 10.2% versus the estimate for 10.5%

Fixed-asset

investment increased 8.1% in the first 7 months of the year,

compared with a projection for 8.9% growth

Aggregate

financing was a two-year low of 487.9B yuan ($73.4B), less than ½ of the estimate of 1T yuan

New yuan loans stood at 463B yuan,

also the slowest pace since Jul 2014 & less than the projected 850B yuan increase

The broad M2 money supply rose 10.2%, the weakest gain since Apr 2015

Policy

makers face a choice: boost demand with cheap credit that risks

undermining financial stability, or curb debt expansion even if that

slows the economy. This data suggests the 2nd option is being

pursued for now. With tepid global demand & domestic businesses

reluctant to invest, the gov has increased fiscal support this

year, even as it held off from further benchmark interest-rate

reductions. The yield on China's benchmark 10-year gov bond

dropped to 2.665%, the lowest since 2006, after the People’s

Bank of China released the money supply data. Underscoring the

economy's dependence on a property market recovery, long-term loans to

households, the majority of which are mortgages, increased more than

the total new bank loans in Jul for the first time since 2007.

Property

development investment in the first 7 months of the year rose 5.3%, while the value of property sales during the period soared 39.8%, the National Bureau of Statistics said. Home sales value rose

41.2% while new property construction increased 13.7%. A

monthly GDP tracker slipped to 6.94% in Jul,

from 7.13% a month earlier. Economists expect the official

growth pace, at 6.7% in Q1 & Q2, will slow

in Q3 & again in Q4.

The

PBOC has held the main interest rate at a record low since Oct.

Policy makers reiterated last week that they plan to

pursue prudent monetary policy. This week, the central bank offered more

signals about its evolving monetary policy stance, flagging continued use of liquidity tools rather than further cuts to interest rates.

The week closes with little accomplished today. Dow is up almost 200 in Aug on unimpressive economic data. The coming weeks, prior to the Labor Day holiday, should not produce much excitement as more traders go on vacation to enjoy profits.

![Live 24 hours gold chart [Kitco Inc.]](http://www.kitco.com/images/live/gold.gif?0.2140593389088844)

No comments:

Post a Comment