This blog gives investors more financial information for very smart investing!

Monday, September 19, 2016

Markets advance as oil rebounds

Dow jumped up 113, advancers over decliners 6-1 & NAZ gained 30. The MLP index added 4+ to the 303s & the REIT index went up 2+ to 350. Junk bond funds crawled higher & Treasuries was marginally higher. Oil & gold each were higher (more on oil below).

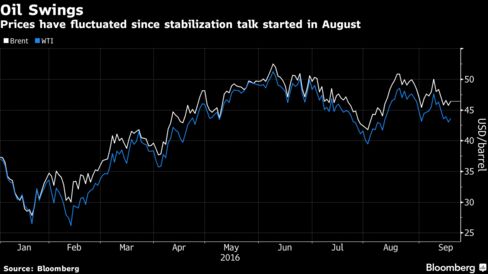

Oil rebounded from the lowest close in more than a month after

clashes halted what would have been the first crude shipment from

Libya’s Ras Lanuf export terminal since 2014. Futures rose 2% after falling 2% on Fri. The tanker Seadelta suspended loading after fighting started Sun between local Petroleum Facilities Guard units &

forces loyal to eastern-based military commander Khalifa Haftar. OPEC

may call an extraordingary meeting if ministers reach consensus at an informal gathering next

week, Secretary General Mohammed Barkindo said.

Oil has fluctuated since rallying in Aug on speculation that OPEC & Russia will agree

on measures to stabilize the market at the meeting Sep 28 in Algiers.

Prices tumbled 6.2% last week amid concern the resumption of shipments from Libya, as well as Nigeria, would worsen a global glut.

The Organization for Economic

Cooperation & Development is urging govs to improve reception

conditions for migrants in order to address anti-immigration backlash. The

Paris-based intl organization recommended countries address the

local impact of the arrival of migrants. The OECD said "large and sudden" inflows of migrants are often

concentrated in the most disadvantaged areas & that govs should

scale up public services in those areas. The organization is also suggesting that countries step up

international cooperation & is urging the intl community to

"significantly increase its effort in terms of resettlement." Migration flows increased by 10% in 2015 across the OECD

area, which is made up of 35 leading industrial countries from around the world.

Investors this week will focus on the Fed's monetary

policy decision & whether economic growth trends have given the central bank reason to raise interest rates off rock-bottom levels. In the days leading up to policy announcement on Wed, market

volatility has spiked following 2 months of relative calm. In the

last 6 trading sessions, the S&P500 has moved at least 1% 4 times, twice up & twice down, whipsawed by shifting

perceptions of what the Fed may do. The CBOE Volatility Index, the most widely followed gauge of near-term investor anxiety, is holding near 2-month highs. If the Fed, as expected, holds off, the focus will shift to its

Dec meeting. Investors were betting such a move was more likely

than not as of Fri, with a 52% perceived probability. The benign rate environment has helped fuel major US stock

indexes to all-time highs in Jul & Aug. The S&P500 now sits

about 2.5% below its record close, & is up 4.5% YTD. The Fed's decision also will factor into the performance of high

div-paying telecoms & utilities shares, which tend to benefit

from low-rate environments. The sectors have each climbed about 13% YTD, topping other groups, but have pared gains in recent

months.

There is not a lot happening in the stock markets. The bears are back in hibernation. The fed meeting at mid week will get the most attention. Prior to that stock prices will fluctuate, driven by various rumors..

No comments:

Post a Comment